The ability to have someone express interest in buying your business is common.

The ability to receive a qualified letter of intent to purchase your business is unusual.

The ability to close the transaction at desired price and terms is priceless.

The closing of an M&A transaction involves great technical skill combined with finesse only gained from years of experience. The orchestration of family, attorneys, accountants, buyers, sellers, and a variety of other important stakeholders would make an orchestra conductor blush. The transaction advisory role requires the ability to be an assertive and forceful negotiator at one moment, and a friendly and comforting advisor the next. While the M&A transaction does not involve life or death decisions, it certainly carries great financial gain or potential harm to one’s business. Yet countless business owners attempt to sell their businesses without proper M&A representation and suffer the greatest risk of all… the lack of certainty that the transaction will close timely and at the price and terms that are acceptable to the business owner.

An M&A transaction can be disruptive to your business. The owner and the leadership of the business are bombarded with significant requests for information, bludgeoned with probing questions, and are travelling down a road rarely or never travelled. The different terminology and perspectives would make a skilled business owner wonder if they ever played the game of business before, and cause them to respond and react much more slowly and cautiously. An often heard phrase on M&A transactions rings loud and true, “Deals do not get better with time”. The role of an M&A advisor is vital to ensuring that the momentum of the deal is maintained and that a delay in timing is not detrimental to the business.

In addition to maintaining momentum and minimizing the risk of time, the other important role that an M&A advisor plays is reducing anxiety and fear. Fear and anxiety are experienced by both the buyer and seller during a transaction by both the buyer and seller. The buyer fears that hidden risks and problems exist and are being withheld during their discovery process. The seller fears that the buyer is going to modify price and terms of the transaction. The legal documentation process involves an important element called representations and warranties. A simplistic summary of this part of the purchase agreement is that the seller will set aside money in escrow to satisfy any representations that are inaccurate or untrue. If the owner tells the truth and properly discloses potential issues, the risk from having a representation and warranty claim is greatly reduced. Sounds simple but this is one area where fear runs rampant… and imagined and unlikely risks get larger.

In a recent transaction, the seller of the business was reviewing his first version of the asset purchase agreement. The fearful topic of representations and warranties emerged and the fear of disaster hit my client like a ton of bricks. The lawyer explained that half of the purchase price could have to be returned if…. my client stopped listening and the blood rushed out of his body. After 20 years of building the business the thought of having 50% of the purchase price returned to the buyer was paralyzing. The lawyer did not know what they said nor the emotional impact on the client until those fateful words left his mouth….. “The sale is off.” The room was silent and binders and folders ready to be packed. I spoke softly and reassuredly to the group and my client. If you tell the truth and present the facts of your knowledge… the risk is minimal. A pulse returned. I explored the likelihood of the events that would cause such a claim and realized that no such event has happened in the past and the likelihood was low of it happening in the future. Lastly, I reassured him that our deal experience and the attorneys’ transactional experience would protect him from this risk. The deal was back on… the blood was flowing again. This is just one example of how fear impacts the M&A process and how important perspective and experience is during the sale of one’s business.

The ability to have a qualified back up buyer provides additional certainty to a seller. Without the fear of competition and potentially not purchasing the desired business, the buyer has the upper hand at the negotiating table. By having multiple offers on your business, the buyer knows that timing, price and terms are not easily renegotiated if they desire to purchase your business. The certainty provided by having other offers in the event that the buyer modifies price or terms is priceless. This certainty only comes from having multiple offers and competition usually provided by a competitive auction process.

Most business owners will claim that the role of an M&A advisor is to make a market for your private business. Many former business owners who have sold their businesses would indicate that the true value of an M&A advisor is the certainty that they provide that a transaction will occur and the desired price and terms.

A buyer is willing to pay a certain amount for a business’ future cash flows, aka Earnings Before Interest, Taxes, Depreciation & Amortization (EBITDA). But, because future cash flows are uncertain, a proxy is needed.

Thus, we have the storied ‘Multiples of EBITDA’ bandied about club locker rooms for decades. Few concepts in finance have generated more confusion or irrational angst. A selling owner once told me,‘Oh, it’s a good price, but I think the multiple is a bit low.’ Really!

***

Multiples of What? Let’s start with EBITDA, which we’ve defined above – or have we?

EBITDA is gross cash flow. It is useful in comparing the earnings (and hence value) of companies because it looks through differences in financing structure (interest), corporate structure (taxes), capital investment policies (depreciation) and the wake of past acquisitions (amortization of goodwill).

Which EBITDA? There is more than one EBITDA candidate to be multiplied. Is it the current year’s annualized? Trailing Twelve Months’ (TTM)? Latest full year’s? In a cyclical industry, the average over the cycle? Since the buyer is buying future cash flow, it is arguable that in a growing business next year’s EBITDA, if supportable, is the most meaningful. If forward-looking EBITDA cannot be convincingly supported, TTM (the most recent actual) is often used.

What Adjustments to EBITDA? What would EBITDA be if another owner operated the business? For example, should there be adjustments (or “add-backs”) for:

Expenses at the owner’s option (‘discretionary expenses’) – e.g. owner compensation and perks above that necessary for capable a hired CEO

Compensation for employees that will not continue under new ownership (net of any replacement cost)

Non-recurring expenses – e.g. a new IT system, major lawsuit, above-market rent to related parties

‘Negative add-backs’ if any; like the loss of a major customer or drop in product selling price (Think Oil) or an owner paid less than market (it happens)

In sum, which EBITDA is used significantly impacts the implied valuation of the business. A business owner ‘talking on the first tee’ rarely mentions, or even thinks about the underlying subtleties mentioned here.

The Multiple bulks up EBITDA into an ‘Enterprise Value’. That is, the value a buyer pays for the cash-free and interest-bearing debt-free business. In either an asset or a stock transaction, the Buyer gets the assets and assumes the normal operating payables and accrued expenses.

How Does the Multiple Relate to Return on Investment? If a buyer pays five times TTM EBITDA and the company generates the same EBITDA next year, the buyer gets a 20% free cash return before deducting interest, income taxes and capital expenditures. If next year’s EBITDA is higher, the buyer earns more than 20%, if lower, vice versa.

So, What Determines the Multiple? Buyer demand, which is based on attributes like predictability of earnings, concentration risk, outlook and synergy. Company size plays into each of these determinants, and is therefore one of the most predictable drivers.

Size Matters. There are break points based on size. Interest from private equity groups begins at about $1 million of EBITDA. A greater number of PE firms are seeking $3 million and more yet $5 million. (Think ‘Return on Bother’) A different set of larger PE acquirers salivate at $10 million. Strategic acquirers need something big enough to ‘move their needle’, so a small business must have something very special – e.g. strong intellectual property, a sizzling brand name, or strong cost synergies (Think plant shutdowns and layoffs) – to attract their attention and fetch a high multiple.

Factors raising the Multiple include strong management, proprietary products or services, pricing power, recession resistance and a growing, defendable market niche.

Factors lowering the Multiple include customer concentration, no CEO successor or weak management bench strength, supplier vulnerability, poor financial records, the inability to forecast reliably and other discernible risks.

What Multiples Are We Seeing? Our firm advises sellers on middle market M&A transactions with $2-to-15 million of EBITDA. Middle market M&A pricing at mid-year 2017 is as strong as it has been in the last 40 years. (“Subject to change without notice”, as they say.) We are seeing today one to three turns of EBITDA higher than prevailed during the downturn of 2008-10.

The take-away is you need to understand what EBITDA is appropriate to use and what value enhancers and detractors apply to the Company. Use Multiples of EBITDA with CAUTION.

Use them as a reality check to test the market reasonableness of company-specific, future-oriented valuation methods like Leveraged Buy Out (LBO) and Discounted Cash Flow (DCF) financial models.

To achieve the highest multiple, and enterprise value, you need to create strong buyer demand – an orchestrated competition among motivated buyers for your business, but that’s a story for another day.

“Do investment bankers add value during an exit process?” Or, in other words, “Are bankers worth their fee?” I am confident that countless first-time sellers have wrestled with this question as they began evaluating an exit. Historically, the answers to these questions were anecdotal. However, a recent whitepaper by Michael McDonald, an Assistance Professor at Fairfield University’s Dolan School of Business [1] attempted (and succeeded) to be the first to take a more scientific approach to determining if and how an investment banker provides value to a client.

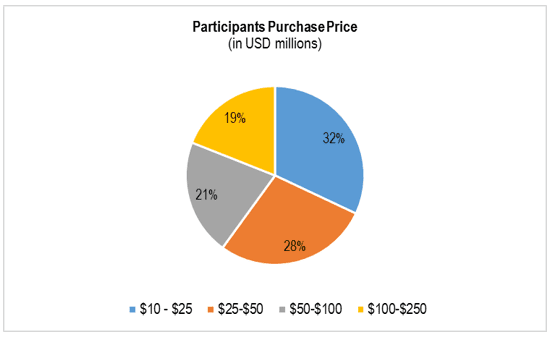

The Fairfield University study represents the first comprehensive independent analysis to determine whether or not sellers valued their advisor, and more importantly, what specific actions and counsel the sellers valued the most. To accomplish this goal, the study used empirical data from 85 business owners who sold their businesses for between $10 and $250 million during the period from 2011 to 2016. All of the sellers used reputable investment banking firms as advisors and the 85 owners accounted for 24 different investment banks. (EdgePoint was one of the investment banking firms that was represented in the study.)

The study’s survey asked the owners a series of questions in an attempt to identify “value”. One set of questions focused on which services the owners valued the most and asked them to rank eight different services (eg, preparing company for sale, identifying and finding the buyer, negotiating the transaction, etc.) The resulting outcome was not a surprise to us at EdgePoint, but I imagine it may be enlightening to owners who have yet to go through the process. The highest ranked service valued by the sellers was, “managing the M&A process and strategy”, closely followed by “structuring the transaction”. Finding the buyer was the lowest ranked service.

The key takeaway is that the M&A process is significantly more complicated and confusing than most first-time sellers realize and an investment banker provides as much value as a guide as he or she does as a broker.

Another interesting finding was that 100% of the respondents said their investment banker added value, albeit in varying degrees. Given three choices (significant, moderate, none), 69% of respondents answered that their bankers added “Significant“ value while 31% answered “Moderate” value. In retrospect, sellers clearly saw the value of having an experienced transaction professional on their team as they structured, negotiated, and ultimately, closed the most impactful transaction of their career.

The Fairfield University study highlighted the valuable role an investment banker provides to a client in an exit process. It also (finally) provides data to help educate and ease the concerns of using an investment banker for first time sellers. With over 250 transactions completed in the past twenty years, the professionals at EdgePoint, are intimately aware of the challenges sellers encounter during an exit process. Our proven track record of successfully closing transactions is grounded in the unbiased guidance and counsel to our clients.

Early on, a senior partner told me, “You know, I never thought much of experience until I got some.”

Part 1 reflected on how emergence of the leveraged buyout, mezzanine financing and the ESOP in the 1970s and 1980s, multiplied transition options for middle-market business owners.

Part 2 reflected on mega-trends influencing business owners, acquirers and transactions as well as memories of The Association for Corporate Growth.

Part 3 concludes with a personal perspective.

Think Grandly of Your Purpose – My life as a merger and acquisition advisor has been 40 years of learning, growing and experiencing afresh. There is no Groundhog Day. It is fulfilling to help a business owner with the most important activity of his or her career: the successful sale or acquisition of a business — that is, the harvest of years, perhaps generations, of creativity and hard work, or the building of a solid platform for future growth.

Taking Care of Business – My first decade in M&A was in a large organization, with staff and support services. That was good, because office technology then was primitive, connectivity as we know it was nonexistent, and daily business activities were far different than today. If you joined the workforce 10 or 15 years ago, it’s hard to imagine the pace of change in daily work routines over the last 40 years.

Since Leonardo da Vinci’s collaborator Luca Pacioli invented accounting in 1494, a pencil (or quill) and sheet of multi-column paper have been used to crunch numbers. I caught the tail end of that era.

Personal computing — using the term loosely — made its appearance in the 1970s. First, came Texas Instruments’ hand-held calculator (which computed present values and other financial necessities), then a Radio Shack TRS 80 (“Trash 80”). Ours housed a Buyer Database, and was the target of a hacker, trying the password “Duran Duran,” (which didn’t work). The laptop’s forerunner, a “luggable” Compaq brand computer, was a drag to haul through airports. Of course, a computer then was an island, not connected to anything else. And, nary a mouse nor an email were in sight. (For more color on computer wiki, read Walter Isaacson’s wonderful book,The Innovators.)

By the 1980s, you could build a spreadsheet using VisiCalc or SuperCalc PC software, and store results on a “floppy disc.” Often, you ran out of disc capacity before finishing, because early floppies held only 80 kilobytes. Later, an improved floppy could store 1.4 megabytes of information.

Before Google, research occurred in a library, and results took days, not an hour or two. Of course, the internet and search engines changed the world in many ways; some profound and obvious, some subtle.

Today, people expect you to do your homework, and they judge you on whether you cared enough to do it. The upside is, with thoughtful use of standard technology like Outlook, you can casually seem to have an awesome memory by asking about family members by name in a phone call with someone you haven’t talked to in years, even if you can’t remember where you parked your car.

Clearly, technology has also changed expectations of appropriate response time. We hear, “I sent you an email an hour ago — didn’t you get it?” Years ago, people had time to think and respond carefully. As psychologist Victor Frankl famously said, “Between stimulus and response, there is a space. In that space is our power to choose our response.” There are times, like during M&A negotiations, when thinking before responding is a definite advantage.

The Bygone Business Lunch – Yes, Virginia, there really was a two-martini lunch, although it was more common with Madison Avenue’s advertising set than on Main Street. Many clients expected a drink at lunch, and expected you to have one, too. The only time I teetered on the edge of inebriation in business, was at the offices of a large London distiller of Scotch whisky. Asked what I wanted to drink, I named their most popular brand. The CFO said in a Highland brogue, “That’s a very good choice.” I’d take a sip, and he’d refill my glass. Fortunately, that was the last meeting of the day.

Life as an Entrepreneur – In 1987, I left the cocoon of a large firm and founded The Trans Action Group, a boutique middle market M&A advisory firm. Thus, I gained a special empathy for anyone who starts a business and meets a payroll. As a friend told me at the outset, “The highs are higher and the lows are lower.”

I learned to treasure loyal friendships. For example, the M&A team at Ernst & Whinney advised Bob Elman, a good friend, on his management buyout of DESA International, and when I left, he was seeking acquisitions. Bob said, “We’ll be your first client,” even before I had formed my legal entity.

Allen Ford, retired Senior Vice President of Standard Oil (Ohio), and Allen Holmes, retired Managing Partner of Jones Day law firm, were friends from our service together on the Case Western Reserve University Board. Allen Ford said he and Holmes were going to rent offices and share a secretary, and asked, “Would you like to join us?” Forget what I just said about the time between stimulus and response. I instantly said “Yes.” Now I had a client and some credibility. Life was great!

DESA was the only name on my first year cash-flow projection to become a client, but other clients came and we cash-flowed positive. Allen Ford did volunteer work on our first transaction, the sale of an ophthalmic equipment business owned by the father of another good friend, Fred Clarke. Allen Holmes gave pro bono legal advice, among other things dictating an indemnity clause so effective it drew admiration from many clients. I was indeed fortunate to have the support of such friends.

The uncertainty of a new enterprise was probably hardest on my wife. She was concerned, committed and supportive, asking daily: “Did you call John Smith back? How was your meeting this afternoon?”

I was on my own with computers — almost. Another good friend, Clint Alston, who ran the Ernst IT consulting practice, sent a young colleague over to help me set up shop, and tutor me in things digital. That’s when I discovered a basic rule of technology: Always go to the youngest person around, when you need help. Recently, the Dean of Case School of Engineering explained why this is so. “You and I are immigrants in the electronic age. Today’s students are natives.”

Each person in a small business shapes the culture. A former colleague, Frank Novak, joined the firm as an owner a year after founding. Over 21 years, we grew The Trans Action Group to seven professionals and closed 75 M&A transactions, 19 of them cross-border. From our offices in The Hanna Building, we also watched the early redevelopment of Playhouse Square and downtown Cleveland.

Time Marches On – In 2007, two key members left the firm (one to buy a business and the other to retire), and I realized I really enjoy recruiting clients and working on engagements, more than the compliance and administrative activities consuming so much of my time. After considering the best path, we chose EdgePoint, a fast-growing boutique M&A advisory firm with the same values and mission: to bring top-quality professional M&A services to owners of middle-market businesses.

I was happy to trade my former CEO duties for those of Managing Director, developing new business and serving clients. I studied for the first time since the CPA exam decades before, and got my securities licenses. Years ago, I waited a month for the CPA exam results by mail. This time, it was a very long minute, staring into a computer screen. Both results were well worth waiting for.

As an M&A professional, it is reassuring that my own M&A transaction was successful, and I continue to enjoy working in an energized small-firm environment.

The “F” Word: Fees – It’s curious. Owners who willingly pay up for a fine piece of equipment may be irrationally fixated on professional fees in an M&A transaction. Fees are earned only when the seller’s transaction closes. For a seller, creating orchestrated competition among motivated buyers generates value far greater than the advisor’s fees. To reinforce the value proposition, we use win-win performance-based fee structures, like an incentive percentage above a pre-agreed value. Value-adding service at each stage and frequent communications create a satisfying client experience.

To illustrate, an owner came to me because his general manager wanted to buy the business. He was willing to sell, but said the offer seemed low. It was. We obtained offers well above what the employee could afford. The outcome was a strategic transaction at twice the original offer, with a key role and phantom stock for the employee. Our transaction fees were not an issue.

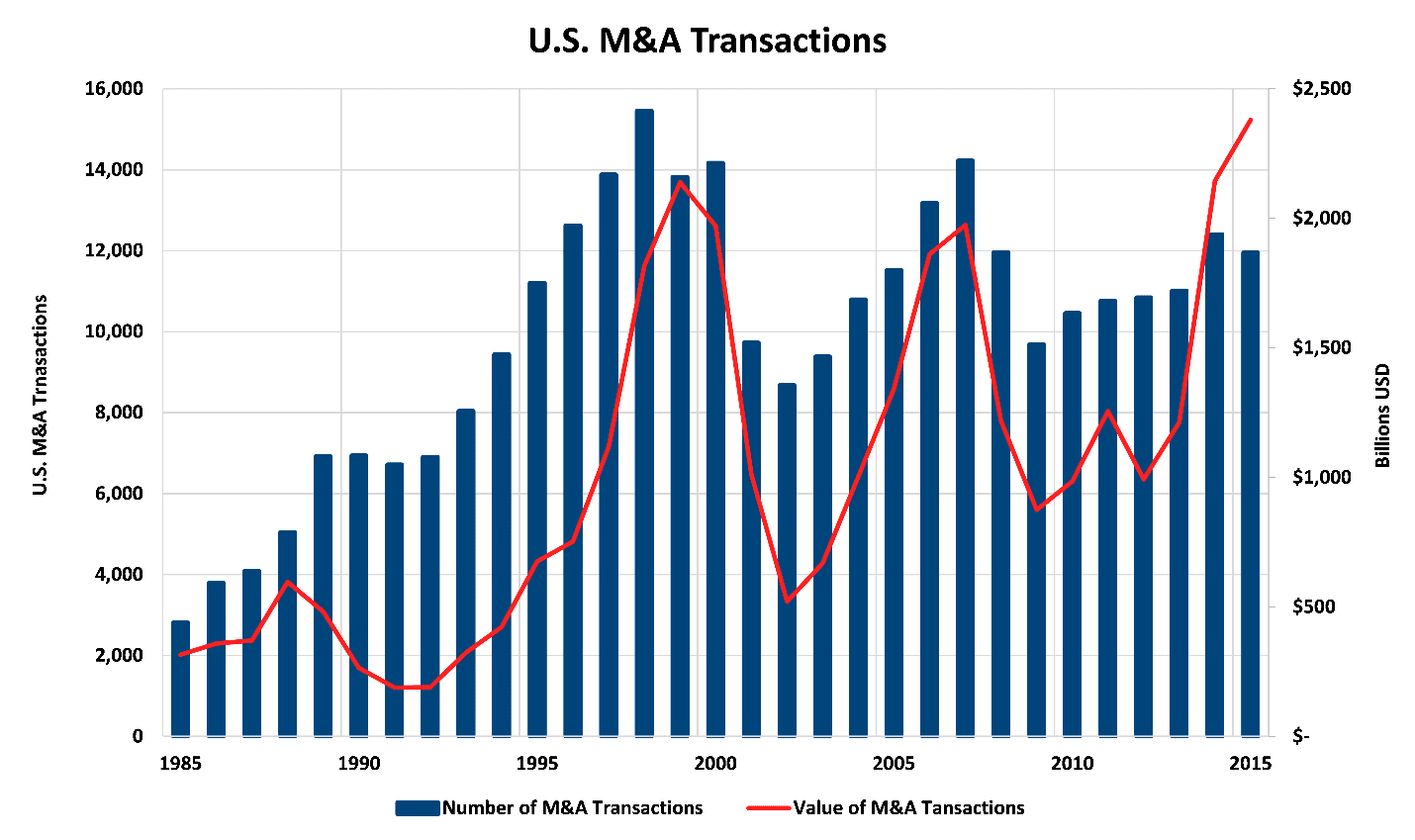

Roller Coaster Ride – As you know, M&A activity rises and falls with economic conditions and financing markets. Over 40 years, it has been quite a ride for owners, acquirers and advisors. The graph below conveys transaction variability since 1985. (Apparently, anything older is prehistoric to the Institute of Mergers, Acquisitions and Alliances, source of this data.)

The smaller-transaction market (think blue bars above) is more stable than mega-deals (dominating the red line) because large transactions are more closely tied to the stock market, and private businesses have strategic and shareholder needs to address, regardless of market conditions. However, many sellers wait too long to pull the trigger. For the owner that misses the “fleeting moment of perfect flavor,” it usually takes at least five years (another growing season) for the fruit to ripen again.

Indelible Clients – While this article is about to degenerate into stories, you also get a “moral” or lesson with each.

Engaged by the Asian Development Bank to improve venture-capital access in five developing economies, we learned there were “Business Development Companies,” which sounded like venture capital firms. Why were they not working? We learned BDCs required collateral, which applicants did not have—so the BDCs made no investments. As it turned out, BDCs were run by former bankers, who continued their old habits. Moral: People can be more important than a business model.

Bob Elman of DESA demonstrated his character a second time. We found a strategic acquisition, and negotiated a Letter of Intentto buy a generator manufacturer. The owner died suddenly before closing. He had told his wife he liked the buyer, so after a respectful time, the deal was on again. Bob said, “I know the business isn’t worth as much without him, but I can’t renegotiate under these circumstances.” We closed on the original terms. That year the hurricane season was intense and DESA sold every generator it had in stock or could manufacture. Moral: Sometimes, doing what feels right can pay.

A client’s president told me during the sale process: “I’m probably the only person in the company that thinks no one else knows what’s going on.” Moral: Confidentiality is very important, but employees seek job security. Working for a company with no visible succession plan is not security.

We sold a Tier 2 automotive-plastic-components manufacturer to a NYSE buyer. The heart of the seller’s operation was a machine with many in-house engineering changes that gave it a competitive edge. The buyer intended to relocate everything to one of its facilities. The seller said, “I really advise you not to move that machine. It has a lot of ‘black art.’” With a seemingly adequate stockpile of parts, the buyer disassembled the machine and shipped it off. They could not make it work right in its new location, and their largest customer ran out of critical parts. Two Morals here: First, buyers should take a seller’s warning seriously. Second, protect your client: the asset purchase agreement had three ways seller could meet earn-out provisions, any one of which required payment—and seller collected, in spite of buyer’s self-inflicted disaster.

What Does M&A’s Future Look Like? – In this three-part article, I’ve tried to convey my take on the Middle Market’s evolution with “thoughtful irreverence.” I hope it’s been illuminating. With no special insight on tomorrow, I eagerly look forward to dealing with interesting new developments certain to arise in our fast-paced business world. I’ll likely need to update this article in a few years—so stay tuned.

Experience is what happens while you march toward the front of “Class Notes” in the alumni magazine

Part 1 reflected on how emergence of the leveraged buyout, mezzanine financing, and the ESOP in the 1970s and 1980s multiplied transition options for middle-market business owners. (read Part 1<)

The Diversity of Ownership – Over the last 40 years, the makeup and motivation of business owners has changed in ways that will affect middle-market M&A for decades to come.

The age at which owners are ready to sell has fragmented dramatically from the 60 or 65 year old transitioning for retirement years ago. Today’s founder may want to sell at 45 or 50 and do something else with the rest of life – maybe start another business, “give back” in nonprofit activity, or seek “life experiences.” Forget the hammock; bring on helicopter skiing and Habitat for Humanity!

Yet, overall, data shows the average age of business owners is increasing. For some, the phrase “80 is the new 65” resonates. People act younger, live longer, work smarter and feel less constrained by past retirement conventions.

Few women ran or started businesses in the 1970s. Gradually, that has changed. As one measure, top MBA programs now have 35 to 45 percent women in their ranks, and gender creep is expected to continue. A 2015 study by Womenable and American Express found 30 percent of all businesses in America are women-owned, and revenues of women-owned businesses have increased 79 percent since 1997.

Similarly, the number of Minority Business Enterprises (MBEs) owned by African Americans, Hispanics and Asians grew 60, 44, and 40 percent respectively between 2002 and 2008, according to the Minority Business Development Agency, as many public contracts and large corporations encouraged more inclusiveness. Many of these MBEs are growing into middle-market companies and beyond.

Many owners of successful businesses today say their children have no interest in taking an active role in the company, raising the need to transition the business proactively to employees or an unrelated party.

Consolidation Pressure Cooker – During the 1990s, owners of smaller U.S. companies in many sectors began to feel increasing pressure (beyond the tendency of mature industries to consolidate) on profits and their very existence, from four long-term megatrends:

Large customers winnowed suppliers to those with critical mass and scope.

The rising cost and pace of technical change required major capital investments more frequently.

Financial buyers launched a wave of strategic initiatives.

The term “Critical Mass” took on a whole new importance. Owners heard, “Get bigger or get out.”

To remain globally competitive, major multinational corporations formed close working relationships with fewer suppliers. It was just too expensive to buy a few items from a whole lot of suppliers. For example, Rubbermaid sought to reduce its supplier base by 80% to achieve a sustainable 15% cost savings. To be a “keeper,” smaller companies had to deliver consistently flawless products, just in time, and be ISO 9000 certified.

Product life cycles and product-to-market cycles became shorter. Each new technological development tended to require a larger investment, and to require such investment more frequently, just to keep up.

Globalization came to the middle market. In 1994, America entered the age of NAFTA, and freer trade globally. Less restrictive trade barriers presented both challenges and growth opportunities, but required more resources from participating companies.

Also in the 1990s, buyers’ strategic “add-on” acquisition initiatives sought more than mere financial return. This meant operational due diligence was more thorough and took longer, but risks to the careful buyer were lower and value-creating opportunities greater.

For all these reasons, many middle-market businesses turned to acquisition, joint venture, strategic alliance or a sale or merger, depending on their situation. “Strategic” became the transaction de rigueur.

Seeking Growth: In the Shoes of The Buyer – The buyer’s view is very different than the seller’s.

A buyer buys the future. “Past performance may not be indicative of future success.”

Forty years ago, articles in the Harvard Business Review and other respected mastheads bore this bleak theme: With hindsight, most acquisitions — yes, most — fail to create value for the buyer’s shareholders. The parade of such articles continues in the 21st Century without let up. Ouch!

A successful acquisition creates sustainable profit growth. The first place a company should look for growth is within its own business—new customers, new geographies, new versions of its products or services. That’s because the more you understand, the lower the risk of failure. But, the desired growth is not always available organically, or it may be faster and cheaper to acquire.

Caveat emptor. To create incremental value, the buyer must have a well-reasoned strategy, understand the acquisition candidate, buy at the right price and terms, and successfully integrate the acquired business into its operations.

In my experience, a successful acquisition begins with “know thyself” and a close understanding of the candidate’s strategic fit and value drivers. Jim Dunstan, CEO turned business professor at UVA’s Darden School, poses two questions: “Why do our customers buy from us?” and “How do we make money in this business?” It is better to overpay (a little) for the “right” business than to land a “bargain” that does not achieve objectives.

What turns a buyer on? Buyers pay a premium for Clarity, Profitability, Predictability and Growth.

Corporate Clarity: An understandable business model with sustainable competitive advantage.

Profitability: A return greater than comparable companies generate.

Predictability: The ability to see future revenues reliably; absence of surprises; pricing power.

Growth: Steadily increasing cash profits over a five-year planning horizon

Many strategic buyers use the private-equity pricing model as their starting point, because that’s where competing financial buyers are. (How much can I borrow, plus how much can I invest for a 25% rate of return?). To that value, they may add a bonus for synergy, depending on how important the “target” (notice the military term) is to their plans, and how strong they perceive competition for the deal. A buyer will share some obvious synergy savings (elimination of some administrative costs) if it has to, but will be secretive about any unique “strategic” synergy. In fairness, that is their value-add, not the seller’s.

Many good acquisitions fail after they close. Why? Because they lack a disciplined plan to adhere to assumptions in the valuation model, or because due diligence was incomplete. (Surprise!) If the valuation depends on closing a facility and moving the business into the buyer’s plant in six months, and it takes two years, the buyer will never see the forecasted return on investment.

The Divestiture: When Less Is More – As Harvard’s Michael Porter says, “The essence of strategy is choosing what not to do.” Companies must be good at pruning as well as planting.

Over the years, divestitures have become respectable, and necessary. Years ago, a divestiture might be seen as a past mistake, or that the company was in financial trouble. That is no longer true. In 2013, a Deloitte survey reported, “corporate divestitures are increasingly being driven by companies’ strategies to focus on growth and shed non-core, low-growth assets, and less by financing needs. As the business focus changes, some assets are worth less to their current owners and more to others.”

Each year many middle-market lines of business, divisions, and subsidiaries are divested. Acquirers actively seek these cast-offs, and win-win transactions can be crafted. Sometimes a business is even re-acquired by its founder.

Cross-Border Transactions – Forty years ago, only large companies, it seemed, were multinational. An ambitious growth objective for a middle-market company was to become national. (What’s not to like about a market of 300 million people, all speaking English?) But, as noted earlier, many companies were dragged into international waters by large customers. Others who had sated a niche market in America found that with a little planning, they could sell their products or services overseas to new customers.

An outbound international initiative for a middle-market U.S. company typically begins with an export program, then an outpost in Toronto, and gradually moves into markets with increasing cultural differences and less modernity, such as Kabul. Well, maybe Kuala Lumpur

Globalization also opened middle-market North American companies with a coveted customer base or unique intellectual property to a range of buyers from Europe, Asia and the Middle East. Today, a strong seller can expect to fetch attractive offers from selected overseas buyers.

Middle-Market Glue – Over the last 40 years, The Association for Corporate Growth has played a key role in bringing buyers, financiers and advisors into a middle-market agora. It is the gathering place.

From a small New York clique, ACG reached 500 members in the 1970s, when I joined. Filling an obvious need, the organization has grown to 57 chapters in 11 countries serving more than 14,000 members of the M&A community.

I have fond memories of attending many an InterGrowth, ACG’s global conference held annually at a posh watering hole in a sunny clime, where we rubbed (and bent) elbows with CEOs of fast-growing companies and other members of the business, financial and governmental glitterati. During the 1981 gathering in Boca Raton, Florida, I made an unplanned day trip to New York. That day John Hinckley Jr. tried to assassinate President Reagan in Washington, and suddenly airport security and air traffic control turned upside down. The President survived, and I returned at midnight, missing the cocktail party I was hosting. One year, Michael Milken — the junk bond king and announced keynote speaker — was a no-show, jilting ACG for his own investor-rich “Predators Ball” event. Post script: In 1990, he pled guilty to felony charges for violating securities law, served time and is banned from the securities industry for life.

When I was ACG President (1995), Richard Teerlink, the accountant-biker CEO of Harley Davidson, won the growth award for an amazing turnaround, and an early example of the resurgence in American manufacturing. We also launched a multiyear initiative to expand international chapters, and chose Diane Harris, head of Corporate Development at Bausch & Lomb, as ACG’s first woman president.

In ACG, friendships form; deals spark. My special long-time ACG friends include Bob Coffey (The Coach, Toronto), Alan Gelband (Gelband & Co., New York), Carl Wangman (ACG Global, Chicago) and Tom Smith (deceased).

Speakers at InterGrowth tell great stories. My favorite is this one, told years ago by Jim Balsillie, Co-CEO of Research in Motion (Blackberry). He was seated near Barbara and George Bush at a fancy dinner. Mrs. Bush told him George was addicted to his Blackberry, so Jim confessed that his wife had a rule that he had to leave his on the foyer table when he came home. One night, he snuck it into his pocket, and went upstairs to read his little daughter a bedtime story. The unseen phone buzzed just before his wife came into the room. Their daughter said, “Daddy just farted.” “Now I had a dilemma,” said Jim, “do I confess to the Blackberry or the fart?” With that, President Bush laughed so hard he sprayed red wine all over the tablecloth.

But Wait – There’s More – In the next issue of the EdgePoint Newsletter, Part 3 will conclude with the advisor’s perspective.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.