By Paul Chameli,

Managing Director

The increased prominence of Private Equity investors and their valuation approach has created a simplified approach to business valuation in the marketplace. Once extensively grounded in a detailed consideration of discount rates, future assumptions about cash flow projections, and appropriate assumptions regarding terminal values, conventional valuation tends to be more focused on valuation multiples of EBITDA (Earnings Before Interest Taxes Depreciation and Amortization). While perhaps adopting this approach to valuation is better for purposes of efficiency, this mindset has the effect of causing sellers and even their investment bankers to take their eye off a critical element of financial theory that can have significant impact to valuation – synergy opportunity. When synergy opportunities exist for a strategic buyer of a Target – or a financial investor that has an existing portfolio company for which the Target can be affixed – the Target has higher intrinsic value to the strategic buyer. As a result, the strategic buyer can in theory pay more to acquire the Target since the benefits are higher than the reported earnings of the Target.

Considering this clear benefit, Sellers and their investment bankers should focus on developing a synergy hypothesis that can be communicated to potential buyers and financial investors. While sophisticated buyers and investors are acutely aware of, and actively seek out these synergy opportunities when pursuing targets, demonstrating to the buyer universe that the Seller is aware of synergy potential will establish the expectation that the benefits of these synergies be inherent in the valuation of the Company.

This write-up is a refresher on common categories of synergy that are available to, and form the basis of, M&A motivation and value creation.

Synergy Opportunities

Cross-Selling

The most common synergy opportunity sought by strategic buyers in an M&A transaction is the opportunity for cross-selling. This is a generally well-understood synergy opportunity, but not one as often communicated by Sellers to Buyer candidates. Cross-selling is, as the name implies, the ability to sell the Buyer’s product to the Target’s customer and vice versa. A strategic buyer will often consider if there are “bundling” opportunities, or the ability to package up multiple logically adjacent products in one package and as a result offer a value proposition to the customer in terms of overall value and perhaps better pricing.

Another common associated synergy with cross-selling is the ability for a sales person with a customer relationship to manage a greater number of products with that one particular customer. So, for example, a pharmaceutical salesman for Pfizer visits a Doctor to present product. As that salesman is walking out the door, a salesman for Merck Pharmaceutical walks in to see the same Doctor. If Pfizer and Merck were to combine, the first salesman could in theory handle both product lines and either rationalize or repurpose the other salesman.

Geographic Presence

Related to the above, but a big enough consideration to warrant its own category, is synergy achieved by localized presence. Because or cultural differences and customs, it may be difficult for an American company to sell product into Germany, or vice versa, without a local on the ground to “vouch” for the foreign company. Because customers tend to buy product from local country personnel, the acquisition of a Target with established local distribution and a local brand is viewed as an opportunity to achieve sales that the Company would not otherwise achieve without the local presence.

New Distribution Channels

Further related to cross-selling is the opportunity for a Buyer or Target to achieve access to a new distribution channel through a combination. Often employed by consumer oriented industries but increasingly employed in other sectors, this motivation gives the Buyer or Target another medium for which to sell product. For example, a brick and mortar retailer that acquires a company focused on e-commerce, or vice versa, has the clear motivation to capitalize on multiple forms of purchasing behavior. In the industrial application, a combination may give one company that has exclusively sold through independent sales representatives (“ISR”) access to a catalog or network of stocking distributors to sell their product, while at the same time allowing the Buyer to access new channels themselves through the ISR network of the Target.

Operational Cost Savings

A significant driver of M&A in the 1980’s, due in large part to bloated middle management ranks, the idea of synergy from significant operational cost savings has largely dissipated in recent decades. Some of this is the result of the fact that many companies operate much leaner than they did in the 1980’s, the fact that technology has already created a lot of those savings, but also because M&A strategists have learned their lesson from the disasters of 1980’s combinations. In those days, large holding companies attempted to overlay a common operational infrastructure over a number of companies, many of them in unrelated industries. Remember Beatrice? Companies like this would establish a common platform for all of its companies, including accounting, customer service, purchasing, etc. This didn’t work as well once business managers learned that operational functionality needs to be tailored for the uniqueness of a business. Most strategic buyers nowadays acknowledge that the operational back office gives the organization a solid backbone for success and that it has to be tailored.

With all of that being said, there are operational cost savings that are commonly sought by strategic buyers – but these are smart strategies that don’t disrupt the operational fabric of the Company. We most typically see strategic buyers attempt to reduce costs through greater purchasing power with vendors or suppliers. Insurance and raw material purchase savings, for example, are achievable when buying in bigger volumes.

Production Synergies

While offshoring to a low-cost country (“LCC”) has been over the past 20 years the biggest operational synergy, a focus on domestic manufacturing in recent years has created a series of new and interesting synergy opportunities, including commercialization of new technologies, domestic production capabilities, ability to capitalize on Buy America credits, and ability to capitalize on excess capacity.

A benefit possessed by a smaller and more nimble organization is its ability to quickly evaluate, commercialize, and integrate new emerging technology into its organization. While larger strategic buyers certainly have the resources to acquire these sort of technologies, they are often not as agile in their integration. For this reason, we often see the expertise in these new technologies as a compelling synergy opportunity for strategic buyers.

While facility consolidation had been a common synergy opportunity, in this environment of limited production assets in the United States we see more often that strategic buyers seek opportunities to push more production into acquired facilities. Or often a strategic buyer who has a history of outsourcing non-core production will seek to preserve the margin loss by moving the production to the acquired Target. While vertical integration has questionable merit in most industries, it can be a synergy benefit that otherwise justifies an acquisition or can enable for higher pricing.

Vertical Integration

While the benefits of this have been debated for many years, vertical integration is a possible synergy category for strategic buyers. Vertical integration, owning either a supplier or a customer, is generally an attractive investment for operations managers who worry about managing the cost of their production supply or want to ensure that they don’t lose a customer. While that seems like a great rationale from an operations strategy, the availability of benefits from a financial perspective are generally absent so long as there is an ability to continue to do business with the customer or supplier. If a company can continue to sell product to a customer, what benefit is there to owning the customer – the only benefit is to prevent a competitor from selling to the customer. In that case, however, the company can simply lower its pricing to stave off the competitor. For these reasons, vertical integration is less common in most industries. That being said, there are certain industries for which vertical integration is deemed to be an attractive synergy from a strategic perspective. For example, controlling the only supplier of a required production technique or product can put a company in an advantageous position relative to its competitors. Or in the case of a foreign company that wants to do business in a country but needs local content (for example, to be compliant with “Buy America” provisions), the acquisition of a customer can have clear benefits that would be otherwise unachievable.

Benefits

The benefits associated with synergy analysis and presentation are clearly valuable. In a recent example monitored by EdgePoint, Wabtec (NYSE:WAB) has proposed to acquire GE Transportation Systems for 13.5x the reported TTM EBITDA of GE Transportation Systems. This value was in excess of the multiple for which Wabtec was trading at that time, and from an objective standard a high value for a cyclical business. However, after taking into account all of the cross-selling and operational synergies, Wabtec calculated the synergy-adjusted multiple to be 9.5x and was able to justify the high purchase price as a result. In essence, the synergy opportunity translated into higher value for the shareholders of GE Transportation Systems.

In a transaction recently managed by EdgePoint, the presentation of synergy opportunities to the buyer universe significantly increased the valuation multiple. The Target, broke financial covenants on its loans and was pressured by their lender to liquidate or monetize the investment. Conventional multiples for companies such as the Target were approximately 6.0x EBITDA at that time, which would have resulted in a valuation that just barely covered the debt balance (wiping out all shareholder investment). The presentation of the above synergy opportunities and contribution margin to a strategic buyer, as well as the competitive process managed by EdgePoint, drove valuation multiples to a level almost twice that amount.

Conclusion

Considering the clear motivation, Sellers with a mind on highest value for their Company should prepare themselves and their investment banker for synergistic pricing by accumulating and documenting the synergy opportunities with potential strategic buyers and be ready to present those ideas as part of the sale process.

© Copyrighted by Paul Chameli, Managing Director of EdgePoint Capital, merger & acquisition advisors. Paul can be reached at 216-342-5854 or via email at pchameli@edgepoint.com

By John F. Herubin,

Managing Director

Our team at EdgePoint has advised and consulted with thousands of business owners throughout our combined careers in preparation for a potential sale. We have guided hundreds of these owners through a marketing and sale process to a successful conclusion. Having accumulated this wealth of experience from interviewing all these owners, we are often asked how we know during our discussions when a business owner is ready to commit to sell their business.

Much like a physician prior to an examination, we ask a series of questions of a prospective seller. Based on our extensive experience, the three high-level questions we ask to determine readiness are whether the market, the business, and the owner are ready.

The easiest question of the three to answer in today’s merger and acquisition environment is whether the market is ready. By almost every measurable metric, with limited exceptions, we have not seen a more favorable seller’s market for at least 20 years. The abundance of investable cash (through private equity, strategic buyers, and family offices), a favorable bank lending environment, historically low tax rates, a plethora of buyers, a positive business climate, and a dearth of quality sellers, have combined to create a favorable “perfect storm” for sellers.

The second question of whether the business is ready is more specific to each individual circumstance. Making this determination is also more quantitative and measurable. Organizing and optimizing areas of the company that will positively impact value include operational, financial, legal, tax, and sales and marketing functions. For example, we can assess and determine whether hiring a key employee or buying a new piece of equipment prior to sale will create quantifiable value. We can also espouse the benefits of upgrading financial statements, identifying key employees, and cleaning up obsolete inventory prior to a sale process. Once the decision to undertake and implement these actions is completed, the answer to our second question is also “yes”.

The third, and most subjective assessment our “diagnosis” entails, is determining whether the owner is ready. There are many emotional, personal, financial, family, employee, community, and legacy related considerations for owners to consider before committing to a sale. Our many discussions over the years have educated us, much like a physician, to listen for specific clues or “symptoms” that we hear often which will lead to a “diagnosis” that the owner appears ready to sell.

We repeatedly hear the following “symptoms” which often indicate that an owner is ready:

Ironically, we have found that age is not necessarily a key “symptom” that indicates readiness. The average age of our sell side clients over the past five years is 54 years old. We are currently representing owners in their 30’s and trying to discern the readiness of owners in their 80’s who are still engaged and having “fun”.

Although not an exact science, there are many additional factors that we assess once we complete our initial discussions with owners. As investment banking “doctors” the above “symptoms”, which we repeatedly hear, often affirm our initial diagnosis of a “ready” seller.

© Copyrighted by John Herubin, Managing Director of EdgePoint Capital, merger & acquisition advisors. John can be reached at 216-342-5865 or on the web at www.edgepoint.com.

By EdgePoint

There are several types of buyers in M&A sell-side transactions. One group is strategic buyers who are companies that are in the industry of the seller, and could either be direct competitors or in an ancillary business that would be complementary with the seller’s business. A second common group is financial buyers, which are typically thought of as “private equity groups” or PEGs, which are a group of investment professionals with capital that typically purchase a portfolio of companies in which they own the majority of the equity, but the management teams actually run the day to day operations of the business.

PEGs actually come in many forms, but the most common is a traditional 10-year fund. 10-year funds are generally a group of investment professionals representing the PEG firm, which acts as the general partner, and they raise capital from limited partners (LPs) such as pension funds, endowments, asset managers, or high net worth individuals. They have a 10-year time horizon to put the committed capital to work and return those funds with profit to the LPs. During that time, they need to find privately held companies to purchase, buy them, grow them, and then sell them all within the prescribed 10-year fund timeframe (with some limited ability to extend). If the fund general partners are successful and make a return for their investors, they are able to raise additional successive funds, and the cycle continues. On average, funds may hold their investment companies for five years due to the timing pressure of returning capital and showing returns early enough to raise the subsequent funds. Because PEG firm professionals make their money from fees for managing and investing the committed capital plus a portion of the upside return on the investments that they make, PEG funds need to continue raising funds or their firm and income streams would end. This means that they have pressure to sell companies that have further growth potential to satisfy their fund timing or capital raising initiatives. Fund professionals lament about how difficult it is to find, chase, bid on, win, and close these investments in good growing companies, only to have to prematurely sell and start all over with a different company that may not have the upside of the one they were just forced to sell.

Because of the time pressure of working within a timed fund, many private equity professionals are choosing to go the “fundless” approach and either raise money on each transaction from LPs that know them from prior investments, or have an alternative source of capital that doesn’t necessarily have the same timing. Evergreen funds recycle the money that is returned to the LPs so that the investment pool doesn’t expire. Funds raised by groups of high net worth individuals may not have the timing pressure as a fund with pension or endowment investors.

Another source of capital that has emerged somewhat recently and been growing in popularity for many of these timing reasons is Family Offices participating in the private equity buyout arena. Family offices are private wealth management advisory firms that serve high-net-worth investors. Family offices can invest on their own or in conjunction with other family offices, usually through a separate “private equity” entity that is funded by the family capital. One big advantage to most family office buyout structures is that they have no specific “hold” period, which means they can hold an investment for as long as there is opportunity for growth and return on investment. Just because they have a theoretically unlimited hold period doesn’t mean that they will hold it forever. Family offices generally have private equity professionals and/or investment advisors running their private company investments and will look to take advantage of opportunistic transactions as well. What separates them from the funds is that they don’t have the pressure to exit prematurely when there is still strong growth in the forecast. They are often considered “patient capital” relative to traditional PEGs. This aspect is appealing to many sellers.

Whatever the source of capital, private equity represents a large and growing opportunity for business owners to partner with professionals experienced in growing businesses. They bring resources both in capital and strategically to the companies that they partner with, and allow the business owners to take risk capital off the table while staying involved in the business for as long as they would like to contribute, and allow them to step out of the company knowing their succession plan is being handled by equity-aligned partners who have helped in this transition many times before.

Common considerations for partnering with private equity when EdgePoint advises business owners include:

Family office backed private equity is strong and growing. A survey of 139 single-family offices from Grant Thornton found that 86% of those that already invest in private equity want to increase their commitments over the next three years. The survey found the median office has $276 million in investable assets, and the 109 offices that have invested in private equity since 2009 have allocated more than $8 billion in capital both in committed capital funds and direct investments. Slightly more than two-thirds invest in funds and just over half invest directly in Companies. Another 29% co-invest with funds directly, but alongside funds. Many family offices were funded by operating businesses that made the family wealthy, so there is a good fit and understanding of business owners. In some cases, there can by synergy or industry knowledge with the family office’s operating business as well.

Whatever the source of capital – committed capital funds or family office capital, private equity represents a flexible and potentially valuable transition option for business owners considering transition. Committed capital funds are abundant and eager to put capital to work and will often be the highest valuation even when in competition with strategic buyers, and can add strategic-like value post-transaction. Because of their longer hold timeframes, family offices provide the flexibility of longer term strategies and organic growth alongside a deep capital provider that may also have knowledge and experience in the industry. Both sources of capital offer a flexible and potentially lucrative transition option, without the perceived competitive issues that come with strategic buyers. This expansion of the buyer universe that has been occurring has contributed significantly to the robust and active sellers’ market that currently exists.

© Copyrighted by EdgePoint. Tom Zucker can be reached at 216-342-5858 or at tzucker@edgepoint.com

By Matt Keefe,

Managing Director

Once a business owner has come to grips with selling his or her business, and once the buyer and seller have agreed to the key terms, then the legal documentation and closing phase of the M&A process begins. Inevitably, the documentation and closing phase can be frustrating and stressful for both the buyer and seller and can cause deals to stall, or sometimes even die. One aspect of documentation that usually creates issues is the negotiation of the escrow amount related to potential breaches of Representations and Warranties, or more often referred to as “Reps & Warranties” (Reps & Warranties is a term to describe the assertions that a seller makes to a buyer in a sale.) Fortunately, there is a burgeoning insurance product that is significantly alleviating the hassles tied to breaches of Reps & Warranties.

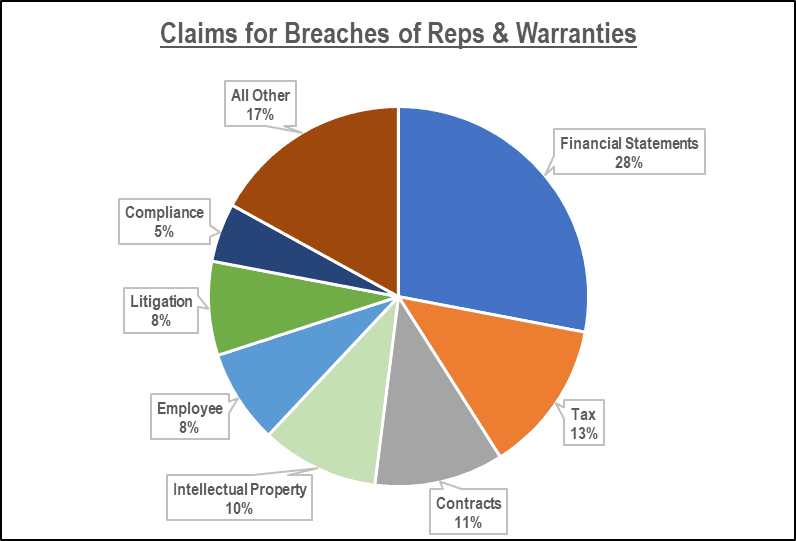

What are typical breaches that would cause a buyer to file a claim and seek compensation? Oswald Insurance, one of the nation’s largest independent insurance brokerage firms, conducted an analysis to identify Reps and Warranties claims by breach type. The results of that analysis are set forth below:

Before Reps & Warranties insurance was available, a buyer of a business would offset a portion of the potential risk related to breaches by asking the seller to hold-back, or escrow, a percentage of the total transaction value. This created a well-defined process whereby the buyer could file a claim against the escrowed amount to recoup a portion of the purchase price if a material breach was found. Typically, the escrow represented 5-10% of the total purchase price and was in place for six to eighteen months.

That was how it happened before Reps & Warranties Insurance came along. Now, Reps & Warranties Insurance is being used in lieu of the indemnity agreements that require escrowed funds. While Reps & Warranties Insurance is not a standard practice in all M&A transactions, the insurance product is being utilize more and more…for good reason.

Reps and Warranties Insurance provides benefits to both buyers and sellers. For buyers, as Chris Jones, Managing Director and Founder of Align Capital Partners, states, “Reps & Warranties Insurance allows us to provide more cash to the seller at closing (making our bid more attractive) and significantly increases the efficiency of legal documentation.” Other benefits to buyers include potential for protection beyond the traditional indemnity period, ability to reduce collection concerns, and the opportunity to augment fraud protection.

Sellers also enjoy significant benefits from Reps & Warranties Insurance. First, like buyers, sellers can reduce legal costs by eliminating the negotiations over post-closing indemnity obligations. Second, and most importantly to sellers, Reps and Warranties Insurance eliminates the need for an escrow, therefore, maximizing the cash proceeds to the seller at closing.

Like any insurance product, there is a cost (premium) for the insurance and that cost is tied to the amount of coverage. The amount of coverage is determined by the deductible limit. For example, in a $100 million transaction, a 10% deductible policy provides $10 million of coverage. The premium can be purchased by the seller and/or the buyer. Premiums are priced based on coverage and are typically 2%-4% of the transaction value. Therefore, the cost of the $10 million of coverage may be $200,000 – $400,000

Since the inception of the Reps & Warranties insurance product, the speed at which a policy can be issued has increased significantly. It typically takes two weeks for a policy to be underwritten. This has also expanded the popularity of the solution

As M&A Advisors, we are always looking for tools to help expedite the process. EdgePoint has closed several recent transactions that employed R&W insurance and found, in all case, the benefits (for all parties) outweighed the cost. To learn more about how EdgePoint uses Reps & Warranties Insurance, or to learn more about EdgePoint’s M&A capabilities, please contact us at 800-217-7139.

© Copyrighted by Matt Keefe, Managing Director of EdgePoint Capital Advisors, merger & acquisition advisors. Matt can be reached at 216-342-5863 or on the web at www.edgepoint.com.