By Tom Stafford, Managing Director

Across HVACR, Electrical, Plumbing, Roofing, Fire Protection, Landscaping, and other adjacent segments of the Facility Services market, private equity (“PE”) backed platforms are “rolling-up” local and regional operators at a pace – and often at valuations – that would have seemed improbable a decade ago. For owners, the opportunity can be significant and very real. So are the risks – particularly for owners who enter the process without proper preparation, competitive tension, or a clear view of what life looks like after closing.

It is not the first time consolidation activity has surged across the building trades. The roll-up era that began in the mid-1990s ultimately faltered, with several high-profile collapses and unwindings that stretched into the mid-2000s. Those outcomes left behind hard-earned lessons about integration, incentives, and capital discipline. The encouraging news is that many of today’s private equity sponsors studied that history closely, and the strongest platforms have built more disciplined, strategic approaches to building facility services companies via M&A.

That discipline matters because this cycle looks less like a passing trend and more like a structural shift. Whether a strategic operator, a public company, or a PE-backed platform, industry consolidators are actively using M&A to reshape how buildings are constructed, maintained, protected, and operated—and it is changing how private owners can ultimately realize value from businesses they may have spent decades building.

When managed well, a sale or recapitalization can produce a premium valuation, unlock liquidity, reduce personal risk, and create the chance for a “second wealth event” through retained equity. When managed poorly, it can become a protracted, disruptive process where the deal never closes—or a transaction that closes but leaves the seller with less autonomy, misaligned incentives, and deferred consideration that never materializes.

[The following is a meant to serve as a high level “guide” to some of the questions owners should be asking before they take the first serious meeting.]

Why Buyers – Particularly PE Buyers – Care about Facility Services.

In this context, “Facility Services” means essential, recurring and re-occurring service providers that install, maintain, repair, or replace critical building systems and exterior infrastructure. HVACR, Electrical, Plumbing, Roofing, Fire Protection, Landscaping, and other specialty trades provide services tied to compliance, comfort, safety, and uptime. The common thread among these, particularly the companies that garner the strongest interest, is non-discretionary demand. Building systems fail, inspections and service come due, and customers need qualified technicians regardless of the macro cycle. The industry’s fragmentation, skilled labor dependence, operational complexity, and strong cash flow potential, are among many of the additional qualities that make these companies especially attractive to private equity sponsors pursuing buy-and-build strategies.

Why are PE Backed Platforms So Active in the Trades Right Now

From an investor’s perspective, the facility services sector combines durability with scalability, resilient demand and an enormous (but not unlimited) universe of potential acquisitions to drive growth. At scale consolidators can leverage both cost savings initiatives and new organic growth opportunities unavailable to local operators. Platforms can centralize dispatch, procurement, and marketing; build national-account capabilities; pursue synergistic growth via cross-selling and recurring service agreements; and add complementary verticals to create multi-trade density that can improve customer retention and increase wallet share.

Ultimately, the most important reason buyers are so actively pursuing owners now, is also the most intuitive. Simply put, larger companies are worth more, in EBITDA multiple terms, than smaller companies. This “multiple expansion,” to create significant value when it comes time for them to exit.

What a well-structured platform deal can do for an owner

For many owners, their business represents most of their personal net worth. A sale converts illiquid, operationally exposed equity into cash—allowing diversification away from labor constraints, weather and seasonality, customer concentration, and regulatory exposure. In many transactions, sellers also retain “rollover” equity, taking meaningful liquidity at close while keeping upside if the platform grows and exits again in the future. Beyond economics, the right partner can bring real infrastructure that is expensive to build independently: recruiting and training, centralized call handling and scheduling optimization, pricing discipline supported by service-agreement programs, purchasing scale across equipment and fleet, and more professional finance, HR, safety, and compliance functions.

Where owners get surprised: valuation, earnouts, and culture

First, be careful not to confuse a “headline multiple” with what you actually keep. Net proceeds can move materially based on working capital targets and post-close true-ups, the treatment of leases and other debt-like items, accrued liabilities, and contingent claims, as well as escrows, indemnities, and survival periods. Two deals can advertise the same EBITDA multiple and produce very different cash outcomes.

Second, earnouts deserve special scrutiny because they can shift execution risk back onto the seller. Payouts may hinge on platform-controlled choices—marketing spend and lead allocation, pricing and discounting policies, system migrations that disrupt operations, or how corporate overhead gets allocated. Earnouts aren’t inherently bad, but without tight definitions, control protections, and a workable dispute process, they can become effectively uncollectible even when the underlying business performs well.

Third, don’t underestimate cultural and talent risk. In facility services, value lives in people. Aggressive changes to compensation plans, routing, brand identity, or local decision-making can drive technician and manager attrition—eroding earnings and customer relationships at exactly the wrong time.

A history lesson: what went wrong in the last roll-up cycle

Facility services consolidation is not new. In the late 1990s and early 2000s, multiple HVAC and electrical contracting roll-ups pursued aggressive acquisition strategies—many of which ultimately underperformed or collapsed. The pattern was familiar: integration was harder than expected, financial controls didn’t keep pace with deal volume, and incentives for founders often broke down once the initial excitement faded. Early consolidators tried to stitch together disparate dispatch systems, pricing models, labor models, and cultures without the operational technology we take for granted today. Public-markets rewarded acquisition volume and short-term optics over operational discipline, masking underperformance. In other cases, rapid deal cadence and inconsistent earnings quality led to painful write-downs and financial distress, while equity-heavy consideration tied to volatile public stock prices created dissatisfaction and retention problems among owner-operators once valuations declined.

Some platforms ultimately entered bankruptcy or were sold at distressed valuations, reinforcing skepticism among long-time operators—and creating a “once burned, twice shy” attitude that still shows up in founder conversations today.

Why today’s PE-backed platforms are different (and what hasn’t changed)

Although history sometimes repeats itself, the current wave of facility services consolidation features genuine structural changes. Many modern platforms bring sophisticated operating playbooks – integrated CRM and dispatch, pricing analytics, and KPI dashboards – all of which were largely unavailable in the 1990s. More robust private markets enable a longer-term approach than the public-market consolidators of the past, tolerating near-term integration costs that can yield multi-year value creation with prudent capitalization and disciplined execution. Finally, diligence and deal structuring have matured, and key stakeholders have become more sophisticated. Quality-of-earnings work, normalized EBITDA frameworks, tighter acquisition criteria, conservative leverage are standard at reputable PE firms. Still, competition and abundant capital can encourage aggressive pricing and “deal momentum,” which is exactly why seller preparation and representation remain critical.

Why going it alone often costs more than the fee

Owners sometimes bypass an investment banker to avoid fees or because a platform approaches them directly through a referral. In practice, that choice often reduces net proceeds and increases risk—not because platforms are “bad,” but because the process is complex and the first draft of terms is rarely seller-friendly.

A strong sell-side M&A advisor creates competitive tension to improve both price and terms, helps you present a diligence-ready earnings story that survives scrutiny, and negotiates the mechanics that drive real outcomes: working capital language, purchase-price adjustments, escrow and indemnity structure, rollover equity governance, and earnout definitions. Just as importantly, a good advisor runs diligence like a project—protecting your time and limiting operational disruption so performance doesn’t dip while the buyer is watching.

In facility services transactions, these “details” routinely swing outcomes by seven figures.

Bottom line

Selling a facility services company to a PE-backed platform can be transformative—but only if the economics, governance, and post-close operating reality match the promise of the headline valuation. The sector’s prior boom-and-bust cycle is a reminder that consolidation without discipline fails. Today’s environment is more sophisticated, but not immune to misaligned incentives, integration friction, or poorly drafted earnouts. If you are considering a sale, the goal isn’t simply to “get a high multiple.” It is to structure a transaction that protects your people, your culture, and your downside—while preserving a credible path to upside through rollover equity. An experienced sell-side advisor can help provide leverage and clarity – and ensure that the deal you sign is a deal that you can actually live with after closing.

© Copyright by Tom Stafford, Managing Director, EdgePoint Capital, merger & acquisition advisors. All rights reserved. Tom can be reached at 216-342-5775

By Chris Duncan, Director, Business Services

Most business owners approaching a sale think the goal is simply to find the highest bidder. In reality, who buys your company matters as much as what they pay for it — and the differences between strategic and financial buyers run deeper than most sellers ever realize.

When owners begin thinking about an exit, they tend to focus on one number: the headline purchase price. It’s a natural instinct. But experienced advisors will tell you that the type of buyer — not just the offer — shapes almost every outcome that matters: deal structure, speed to close, what happens to employees, how earnouts are calculated, whether your legacy survives, and how much of that headline number you actually take home.

Strategic buyers and private equity firms are fundamentally different animals. They have different motivations, different time horizons, different decision-making processes, and different definitions of what makes your business valuable. Owners who don’t understand these distinctions going in often leave money on the table, accept terms they shouldn’t have agreed to, or end up in post-close situations they didn’t anticipate.

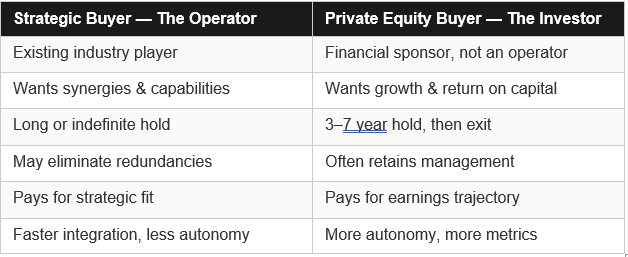

Who is each buyer, really?

A strategic buyer is an operating company — often a competitor, a customer, a supplier, or someone in an adjacent market — that acquires your business because it fits into something it’s already doing. It wants your customers, your technology, your team, your distribution channel, or your geography. It’s buying capability or market position, not just a financial return.

A private equity buyer, by contrast, is a financial investor. It raises capital from institutions and wealthy individuals, deploys it into businesses, works to increase those businesses’ value, and then sells within a defined time frame — typically three to seven years. It is not an operator building a forever business; it is an investor managing a portfolio with return targets and fund lifecycles.

The valuation misconception

The most common assumption owners make is that strategic buyers always pay more. In some cases, this is true: a strategic acquirer can justify a higher purchase price because it’s capturing synergies — the cost savings or revenue gains that come from combining two businesses. For example, if merging your customer base with its eliminates $5M in overhead, it can bid that value into your price.

But the picture is more complicated. First, synergy estimates are notoriously optimistic and frequently don’t materialize on the schedule the acquirer projects. Second, strategic buyers often want to pay for those synergies themselves — not hand them over to you. Third, strategic buyers may discount the value of parts of your business that don’t fit their models, even if those parts are profitable.

“The highest headline number isn’t always the best deal.

A strategic’s price may come attached to earnouts, escrows, and integration terms that erode real proceeds significantly.”

Private equity buyers, meanwhile, are often more disciplined and consistent in their valuation methodology. They’re applying a multiple to your EBITDA, adjusted for quality of earnings, customer concentration, management depth, and growth trajectory. If your business is growing cleanly and the financials hold up in diligence, PE can be a very competitive buyer — especially in a strong M&A environment in which fund capital is plentiful.

What each buyer is really buying

A strategic acquirer is buying the outcome your business produces for it. If your proprietary software reduces its cost-to-serve by 18%, that’s what it’s paying for — not your revenue, not your team, not your brand. This means it’ll value certain assets highly and others not at all. Expect deep scrutiny of customer contracts, technology ownership, and competitive moat.

A PE firm is buying a financial asset with a predictable return profile. It wants stable, growing cash flows; a defensible market position; and a management team capable of executing a growth plan without the fund’s daily involvement. It’s sizing up how much debt the business can service, how many adjacent acquisitions could be bolted on, and what exit multiple a future buyer might pay in five years.

This means it’ll stress-test your EBITDA margins, your customer retention, and your dependence on any single person — including you, the founder. If the business doesn’t run without you in the room, it’ll either price that risk into its offer or ask you to stay and manage through it.

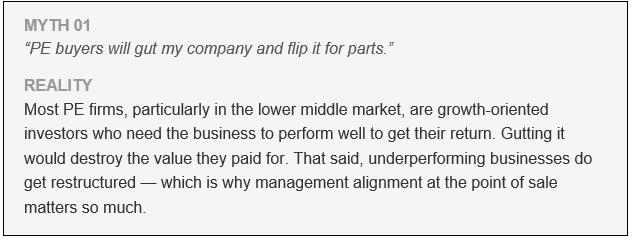

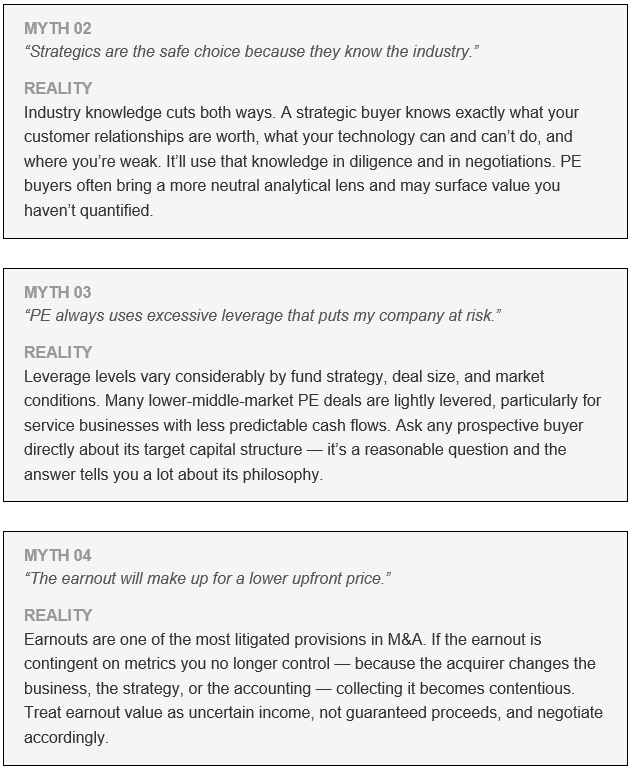

Common myths — and the reality behind them

The question of legacy and people

For many owners, particularly founders, the fate of employees and the continuation of company culture are as important as purchase price. This is an area in which strategic and PE buyers diverge sharply — and in which sellers often have more negotiating leverage than they think.

Strategic acquirers frequently consolidate operations post-close. If they already have a finance team, an HR department, and a regional sales force, they may not need yours. Positions get eliminated. How quickly and how broadly depends on the acquirer’s integration approach, but sellers should ask specific questions: What happens to the existing leadership team? Will this location remain open? How long before we’re fully integrated?

PE firms, particularly those backing a management-led buyout, tend to retain the existing team — at least initially — because that team is part of what they’re buying. Turnover post-close hurts performance, which hurts returns. They have a financial incentive to keep people in place. That said, if performance targets aren’t met, management changes do happen, and they can be abrupt.

“Neither buyer type is inherently ‘better’ for your people.

The answer depends largely on the seller’s circumstances, including motivation, goals, objectives, and overall involvement in the business.”

Speed, process, and deal certainty

Strategic buyers can move fast — or incredibly slowly. A corporate acquirer requires internal approvals, board sign-offs, and sometimes regulatory review. Strategic logic can become political inside a large organization. Deals that seemed certain have fallen apart after months of exclusivity because the acquiring company’s priorities shifted or a new CFO came in with a different view of M&A.

PE firms, by contrast, are in the business of doing deals. Their entire organizational structure is built around closing transactions efficiently. Experienced PE sponsors move through diligence in a defined process and are generally more predictable about timelines. They’re also more experienced at the mechanics of deal-making, which can reduce friction in negotiating the particulars of a transaction.

Deal certainty matters. A slightly lower offer from a buyer with a high probability of close is often preferable to a higher bid from a buyer who might walk away over a diligence finding or who requires three layers of internal approval. Your M&A advisor should be helping you score the full picture — not just the price.

How to think about the two paths

There is no universally correct answer about which buyer type is right for your business. The answer depends on your goals: Do you want maximum liquidity now or continued participation in future upside? Do you care about preserving the brand and team? Are you ready to exit entirely, or do you want to stay involved? Are you optimizing for tax efficiency, deal speed, or certainty of close?

Some sellers run a dual-track process, soliciting interest from both strategic and financial buyers simultaneously. This creates competition that benefits the seller and provides market clarity about relative valuations. Done correctly, it maximizes optionality. Done poorly — with inconsistent messaging or inadequate preparation — it can create confusion and erode confidence in the process.

The most important thing is to enter the process with clear eyes about what each buyer type is optimizing for. Strategics are buying synergies. PE firms are buying returns. Neither is doing you a favor. Both are disciplined capital allocators who will negotiate hard and walk away from a bad deal. The best outcome for sellers comes from understanding the buyer’s perspective well enough to speak its language, meet its concerns, and structure a transaction that works for both sides.

Your business represents years — possibly decades — of work. The buyer selection process deserves at least as much rigor as the business itself received.

© Copyright by Chris Duncan, Director, EdgePoint Capital, merger & acquisition advisors. All rights reserved. Chris can be reached at 216-342-5754