By Tom Zucker,

President

Cleveland, Ohio; January 22, 2018 – EdgePoint, a boutique investment banking firm located in Beachwood, Ohio, announced the appointment of Tom Stafford as Managing Director. In this role, Tom will be responsible for advising the firm’s clients in matters related to mergers, acquisitions and financing transactions.

Prior to joining EdgePoint, Tom spent nearly 14 years at KeyBanc Capital Markets, Inc. as a senior banker in the Mergers & Acquisitions and Financial Sponsor Groups. During his tenure at Key, Tom worked closely with privately held and publicly traded companies, leading the execution of middle market transactions across a range of industries, with an emphasis on businesses in the Industrial, Energy and Infrastructure sectors. His financial advisory experience includes buy and sell-side M&A transactions, public company mergers, fairness opinions, corporate divestitures, as well as a variety of debt and equity financings. With 18 years of investment banking experience, Tom brings a strong track record in executing middle market transactions.

“We are delighted to welcome Tom Stafford to the firm. Tom’s senior level expertise executing sell-side advisory transactions is an ideal fit for EdgePoint. Tom’s consultative approach to serving closely held businesses compliment his deep expertise and experience.” Said Tom Zucker, President and Founder of EdgePoint.

Mr. Stafford earned his MBA in Banking and Finance with distinction from the Weatherhead School of Management at Case Western Reserve University and earned his BA from the University of Michigan.

“The EdgePoint client centered service model and the strong market presence was compelling to my decision to join the firm. I am excited to be part of the EdgePoint team and to continue the significant growth of the firm. I look forward to building upon the momentum that Tom and the team have created,” said Tom Stafford.

EdgePoint specializes in advising middle market businesses and owners regarding mergers, acquisitions, management buyouts, and corporate divestitures. EdgePoint completed more than 20 transactions in the past 18 months. The firm has nineteen professionals.

EdgePoint is a registered broker dealer and a member of FINRA.

Contact:

Tom Zucker, President | 216.342-5858 | tzucker@edgepoint.com

Tom Stafford, Managing Director | 216.342.5775 | tstafford@edgepoint.com

By Tom Zucker,

President

During my thousands of conversations with closely-held business owners over the years, the most frequent question they ask is when to sell their business. Nowadays, nearly every M&A professional heralds the positive attributes of the market as an ideal time to sell a business. Low interest rates, favorable capital gains tax rates, business confidence, and demand pursuing acquisitions are just a few indicators that now may be a good time to sell. From a purely financial perspective, the decision to sell seems like an easy one. Unfortunately, for M&A advisors, the answer to the question of when to sell is not always so easy. Selling a family-owned business often involves a multitude of emotions, and other reasons that are often much more important to resolve than the financial considerations.

Based on more than two decades of advising closely held business owners, conversations around three distinct themes may help clarify emotional or non-financial factors to determine “when” is the optimal time: (1) defining what comes next; (2) determining whether the next generation is ready; and (3) identifying unfinished business.

Defining What Comes Next

A business owner’s position in the company and his or her life purpose often intertwine. To be sure, decades of leading a private company, and receiving accolades and prestige for one’s business accomplishments, is alluring. Countless books and seminars have addressed the idea of defining a compelling future and vision for the second half of one’s life. Unfortunately, many business owners missed those seminars and never read the right books. They were too busy growing and operating their business. The emotional preparation required of owners and their families for life after business ownership is a significant weakness of many business owners’ planning process. Without a compelling future to pursue, the decision to sell becomes strictly a monetary decision, which comes with the risk of disrupting a delicate family, emotional, and life balance.

I recall a conversation with the owner of a precision machining business. He founded the business in his mid-fifties, following a successful career at a similar business. In addition to building an outstanding business, the owner’s religious faith was the foundation of his business and personal life. For several years, his financial advisor had explored and clarified his charitable interests and post-ownership desires. In the owner’s final decades, he wanted to focus on his church and his family. The construction of a new chapel and establishment of missionary trips was his objective. He also wanted to help unify his family by funding exciting family vacations with the extended family. Hardly earth shattering, but for him it was clear, well defined and aligned with his values. I revisited with him a decade after he sold his business, then entering his eighties, and he reflected on his time in business and afterward. He shared with me that his family was stronger than ever and that the proceeds from the sale of his business helped to fund many missionary trips and even a multi-million-dollar chapel for his church. He was truly fulfilled and satisfied with his past decade and spoke with excitement about the future. He shared with me something that he hoped I would share with others: that he wished he had sold his business sooner. His years following the sale were more fulfilling than any other part of his life, and he realized that the value he needed to fulfill his objectives was far less than the overly conservative estimates. His prior planning enabled him to pursue this path with greater confidence.

Determining Whether the Next Generation is Ready

The desire to transition one’s business to the next generation is compelling and often-desired outcome for a business owner. The education, training, and experience required to prepare the next generation for owning and leading the business can seem daunting. Unlike the previous generation, the children of business owners are less willing and capable to assume the leadership role. Further, many children today would prefer jobs in more glamorous industries. An unprepared son or daughter is often a reality for business owners who hope their children will run the business in the future.

We assisted one business owner on his journey as he faced this transition issue. His son, then in his late twenties, had pursued a career in an industry outside of the family business. After several years, the father persuaded the son to return home and join the family business. The son quickly learned the lesson that respect is earned and not given. The son’s progress was not conforming with the owner’s timetable. After reviewing the owner’s options with him, we decided that a minority recapitalization with a financial buyer (i.e., a private equity group) would achieve the desired liquidity while also providing a group of skilled business operators and a formal corporate structure to assist in his son’s development. The recapitalization was a success; the father received enough capital to satisfy his retirement goals and, with guidance from the new partners, the son advanced into a skilled business operator and successfully repurchased full ownership seven years later.

Identifying Unfinished Business

For owners, the ability to grow a business to a certain revenue level, achieve a targeted sell price, or reach another qualitative goal are just a few achievements that justify waiting to sell the business. Whether it is pride, ego, or simply a drive to excel, these reasons are often important to a business owner and can delay or obscure the best time to pursue a sale.

I vividly recall a conversation with a chemical distributor about a decade ago. Although the business was performing well and the M&A market was attractive, the owner was not ready to sell, citing unfinished business. Puzzled, I inquired further as to what was left to accomplish. He shared a conversation with his former employer about the day that he left to start his own company. In his parting words to his former boss, he exclaimed, “I will grow my business to be larger than yours!” This emotional promise to his former employer served as a motivational driver throughout the history of his company. When I spoke to him, his company’s revenue was within $5 million of exceeding his goal. He decided to wait to sell his business in the fall of 2007, based upon this emotional rationale. Unfortunately, the recession hit his industry hard and his business and leadership teams were unequipped to handle the tumultuous ride. The company filed for bankruptcy protection two years later, and he was out of business just a short time later. The bitter lesson illustrates how sometimes emotional or non-analytical goals are obstacles to properly timing a sale.

These stories illustrate just a few of the non-financial considerations that owners face when making the decision to sell their business. From the self-actualized owner to the prideful and bankrupt owner, it is evident that a skilled advisory team is necessary to navigate these risky waters.

© Copyrighted by Tom Zucker, President of EdgePoint Capital Advisors, merger & acquisition advisors. Tom can be reached at 216-342-5858 or on the web at www.edgepoint.com.

By EdgePoint

The tax reform signed into law December of 2017 includes lower federal tax rates and several new tax deductions that apply to both C-Corporations pass through entities, including LLCs and S-Corps. Along with those tax deductions come a new set of restrictions on other deductions such as the ability to deduct state and local tax (SALT) against federal income tax, limitations on deducting interest on business loan payments, among other miscellaneous complicated new rules affecting business taxation.

It is difficult to determine what the effect of these new rates, deductions and limitations will be on a business without examining the unique aspects of the individual company, including what business activity it conducts, its asset and wage base, and its ownership since the new rules were targeted to encourage certain types of business activities over others. How this may affect a business owner looking to sell his/her company is further complicated by the lower tax rates on C-Corps that still carry a double tax on the sale of assets, and the promise of lower taxes on pass through entities that seemingly bring the income tax rate closer to the capital gains rate mostly enjoyed on a sale of the business. With all the counterbalancing built into the new tax law, it is important to review some of the key points of the new tax law to determine how this may impact an owner’s decision to sell.

Corporations and pass through entities will all benefit by having lower actual tax rates. C-Corporations rates drop to 21% and the top individual federal rate of 39.6% goes to 37%, with higher thresholds that save an individual over $31,000 on the first million dollars of income without considering any deductions. Additionally, amounts for bonus depreciation are increased significantly, allowing companies to deduct both new and used equipment purchases. Finally, there is a pass-through income deduction of 20% on Qualified Business Income (QBI) under 199A that applies to businesses not in a specified service or trade company. This 199A pass through deduction reduces K-1 business income by up to 20%, but is limited by several factors including how much W-2 wages the company pays and the amount of its gross depreciable assets.

On the limitations side, the SALT deduction is limited to $10,000 and business loan interest is limited to approximately 30% of EBITDA and phases down to approximately 30% of EBIT in 2022, which will lower the ability to deduct interest further. The 199A pass through deduction of 20% on QBI in the highest tax bracket is limited by 50% of W-2 wages or 25% of Wages plus 2.5% of gross depreciable assets. Thus, the deduction benefits lower income companies that may have more wage or asset intensive businesses, and is either non-existent for some service businesses or reduced for eligible businesses that happen to have high margins that make a commensurate high return on assets or labor.

Entity choice will continue to matter to business owners as C-Corps may have a lower effective tax rate than pass through companies, but are still double taxed on the sale of its assets resulting in an approximate 37% effective rate in no-tax states to higher than 45% for mid-taxed states. This is still better than double tax rates as high as a combined 58% before the tax reform. As most of sale transactions are taxed as “asset transactions”, pass-through entities such as S-Corp and LLCs will continue to be the clear tax choice for those owners looking to sell their companies. This is in addition to the fact that pass through entities will create tax basis (AAA) for their owners on the after-tax income that is not distributed, unlike C-Corp owners who do not benefit in that way.

From a tax rate perspective, pass through entities that qualify for the 199A pass-through 20% deduction and are not limited by any of the wage or asset tests will bring their federal rate down from 37% to 29.6% by applying the 20% deduction to their business income. Even so, the loss of the state deduction in the SALT limitation will add close to 2% additional effective taxes on a mid-level tax state resulting in a 31.5% effective comparable rate. Although this is down from the 39.6% top rate prior to the reform, most higher profit businesses will not qualify for the full deduction, and the best-case scenario income tax rate is still significantly higher than the capital gains rate of 20% on the sale of the goodwill of a pass-through entity. Therefore, when you capitalize earnings on a multiple of EBITDA, which is higher than taxable net income – especially when reduced by Capex and working capital reinvestment, owners will find that they simply cannot “work a few more years” and make what they would in the capitalized sale transaction taxed at predominantly capital gains.

The M&A professionals at EdgePoint have been doing transactions through several major legislative tax changes, and although the change at the time may seem to affect a business owner’s decision to sell, it is our experience that taxes are only a part of the decision. In fact, tax changes generally have not played a major role in our clients’ decision to sell, except to the potential accelerating by a few months during a known tax increase period such as the expiration of the Bush tax cuts in 2012.

In our experience, business owners make the decision to sell when they feel they are ready to have the transition/succession discussion, the market cycle is favorable to them, and when their businesses are doing well. The tax cuts in the tax reform act of 2017 should add fuel to an already accelerating economy, and extend the market cycle to allow savvy business owners to take advantage of the current high valuations for their companies, while hopefully getting some tax relief in the process. That, we believe, will be the true impact of the new tax legislation.

© Copyrighted by EdgePoint. Tom Zucker can be reached at 216-342-5858 or at tzucker@edgepoint.com

By EdgePoint

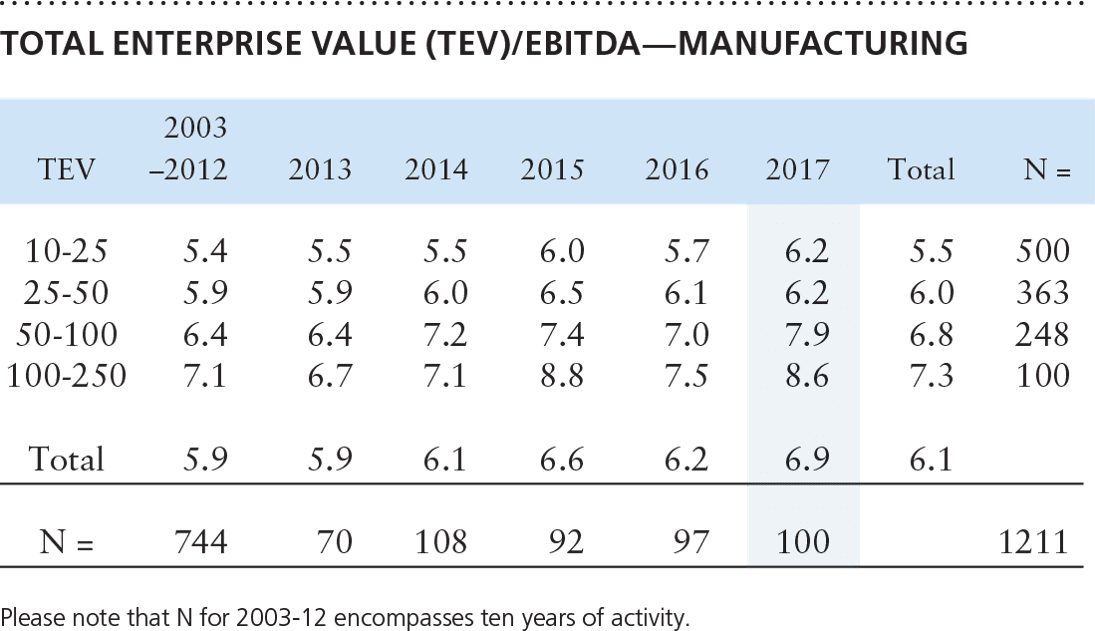

The pricing multiples shown below are averaged multiples of EBITDA paid by private equity groups for privately owned manufacturers in each range of Total Enterprise Value. In addition to identifying general pricing trends over time, the multiples can be useful in developing a ballpark estimate of a company’s market value. However, using them as a valuation tool requires an understanding of composition of the chart provided by GF Data® and adjustments that should be made to both EBITDA and the published benchmark multiple.

The multiples are derived from transaction information provided by two hundred and fifty-seven private equity groups on a blind and confidential basis. They are based on the selling companies’ Trailing Twelve Months Adjusted EBITDA. Only multiples ranging from 3 to 15 were used, essentially eliminating venture or distressed transactions in order to provide consistent information involving mature, profitable companies.

Total Enterprise Value or “TEV” in the far-left column of the chart is comprised of both the equity and the debt in a company, like the equity plus the mortgage in a house. It also includes a likely adjustment for the amount of working capital needed for the company to operate in the manner in which it had operated prior to sale. As evident, the larger the TEV, generally the larger the resulting multiple.

EBITDA or Earnings Before Interest, Taxes, Depreciation and Amortization was “adjusted” in each transaction by adding back extraordinary and non-recurring expenses. An adjustment was also made to executive compensation by adding or subtracting the amount by which it was above or below the estimated market rate of a professional manager. As indicated, among the 100 manufacturing companies acquired in 2017, those with selling prices between $10 million and $25 million as well as those with selling prices between $25 million and $50 million sold for an average of 6.2 times their adjusted EBITDA.

Estimates of value using market multiples are accurate only to the extent that comparative data are used from the sale of comparable guideline companies. Adequate data from enough truly comparable companies are very difficult to find. Given a reasonable number of transactions, GF Data’s disciplined approach to gathering and evaluating data together with its use of averages can provide a credible vehicle for benchmarking. This is because private equity groups are remarkably consistent in the core qualities they seek in a prospective acquisition:

Assuming that the qualities above were largely present in the companies acquired at an average multiple of 6.2 times adjusted EBITDA in the $10 – 25mm TEV size range, they can be used as guidelines to estimate a selling multiple for a prospective seller in the same value range. For instance, a non-proprietary contract manufacturer in a highly competitive market may be expected to command only a 4.5 selling multiple even though it has most of the other attributes cited above. Further adjustments may be needed depending upon prior years’ performance or even anticipated future performance – to the extent that anticipated performance can be credibly defended. Should, for instance, a 20 percent growth in EBITDA during the Trailing Twelve Months be sustainable, boosting the 4.5 multiple to 5.5 would likely make sense provided that the percentages of sales to the larger customers would stay in balance.

The final step in selecting the appropriate multiple to apply to adjusted EBITDA involves evaluating the composition of the subject company’s balance sheet and how it may have changed over the past several years. Inventory and receivables management practices, for instance, can have significant effect on cash flow and thereby could necessitate further adjustments.

As may be evident, one needs to have a lot of experience within the private merger & acquisition market to be able to make the appropriate adjustments to a benchmark multiple. The resulting estimate of market value can be useful to a prospective seller, but it is still an estimate and best used in conjunction with other valuation methods.

© Copyrighted by EdgePoint. Tom Zucker can be reached at 216-342-5858 or at tzucker@edgepoint.com

By EdgePoint

When a business owner decides to sell their Company, an important decision must be made regarding real estate owned in the business or by a related entity. Selling business owners typically face three options:

Whether a business owner decides to sell the real estate at the time of their business sale depends on several factors:

The Seller’s risk assessment and risk appetite are important initial considerations. If a Seller determines to divest the real estate with the business transaction, they may reallocate and diversify the proceeds into new market-based investments that may be more suitable, since the real estate asset may make up a larger allocation of their net worth than appropriate. Diversification is preferred by many Sellers as the perceived risk increases after they cease to have full control over the business which is usually the single tenant. Being reliant upon a single tenant, where business failure or facility migration may initiate an unknown period without lease revenue (depending on the lease or ability to secure a new tenant), may exceed a Seller’s risk appetite. Additionally, the value of the building at the time of the business transaction may be one of the highest because the Seller can use the business transaction to extract favorable lease terms or values from the business buyer, and the original lease term is generally the longest at the point of the original signing of the lease – which generally leads to a higher value.

Sellers preferring to maintain ownership of the real estate must consider the ability to procure a mortgage with interest rates and terms that may be different than an owner-occupied mortgage. If a Seller reduces their ownership in the business below 50%, the real estate generally becomes an “investment property”, and may be subject to higher interest rates and more restrictive terms, and some banks don’t offer those mortgages. Owner-occupied mortgages typically feature lower interest rates and more favorable terms (length of amortization, loan to value, etc.).

Sellers must determine whether market timing is optimal. Oftentimes, simultaneously selling the business and real estate is the most advantageous time to sell because a new longer-term lease can be negotiated as part of the business transaction. Even if the business buyer is not purchasing the real estate, the new lease that is negotiated during the business transaction can provide a third party sale-leaseback investor group with a longer lease with which to value the real estate. Because a longer lease term provides more certain and longer cashflows, banks will give these real estate buyers longer amortization (and sometimes higher loan to value) for their mortgages in order to purchase the real estate. Higher low-cost leverage and better cashflow due to the longer terms, allow real estate buyers to pay more for a building because the bank leverage increases their equity returns. Since the lease term will probably never be longer than when the lease is originally signed, this may be the best opportunity for an owner to sell its real estate.

Inversely, if a Seller determines that the timing is not yielding the desired value, they may opt to keep the property and collect rental income or sell to a third party in the future. This scenario presents potential risks to future value because lease terms and future cash flows, which Real Estate Investors use to generate values, may not align with financing secured to purchase the property. Most lease extensions are not as long as the original lease, which may make longer-term financing more challenging for a future buyer. Market timing must be considered in conjunction with the financing options that may be available currently that would also influence value.

A third-party sale-leaseback arrangement, which can be arranged by a commercial realtor, investment banker, or, sometimes the business buyer, can represent the best opportunity if the business buyer is not open to buying the real estate themselves. A sale-leaseback is a real estate transaction consummated with an unrelated third-party (real estate investor), preferably concurrently with the business transaction. The real estate investor enters into a lease agreement with the new tenant (business buyer). A real estate investor can maximize the value received by the Seller, and both of the transactions are completed for the Seller. The real estate investor benefits from the favorable terms (discussed previously) negotiated into the new lease, and the business buyer has an agreeable lease and is not required to own real estate, as may be their preference.

Deciding between a real estate sale or lease/own arrangement may depend on the Seller’s investment horizon. The Seller must determine whether they would maintain the investment long enough to realize an advantageous return over an acceptable time period versus an immediate sale with reinvestment of the proceeds. Shorter to intermediate-term investment horizons typically provide an advantageous return if the real estate is sold concurrently with the business. Sellers must also consider the liquidity of real estate compared to other market-based forms of investments as it relates to their risk profile and retirement income needs.

Common to every transaction, tax consequences should be considered carefully. If the real estate is sold at the time of the transaction, the Seller will likely incur tax at the capital gains rate, which is currently at 20% federal. Additionally, the Seller can reinvest the post-tax gain into other assets immediately. Inversely, if real estate ownership is maintained and leased to the Buyer, rental income is treated as ordinary income, and the tax rate is currently around 40% (highest income tax rate for individuals is 39.6%), with no deduction for principal payments on mortgages.

The investment horizon and tax consequences are best demonstrated in the example below with the following assumptions:

First, calculate total net proceeds if the Seller chooses to divest the real estate concurrently with the business. In this example, the net after tax and debt proceeds are $500 thousand if the property is sold for $2.0 million with capital gains tax treatment, a state income tax rate of five percent, and $1.0 million remaining on the existing mortgage.

Alternatively, if the real estate is held post-transaction and leased to the Buyer using a triple net lease (tenant agrees to pay all real estate taxes, building insurance and maintenance expense), the Seller will receive cash flow after tax and mortgage payments of approximately $27k annually.

From the two calculations above, the estimated payback period of the net proceeds can be compared for an immediate real estate sale versus the lease model by dividing the real estate sale proceeds by the annual rental net cash flow, which is illustrated below:

![]()

As illustrated above, the Seller would break even on cashflow after 18.5 years. Reinvesting sale proceeds at a 4-5% conservative market return would extend the payback period to well more than 20 years on a. Of course, holding real estate indefinitely can return a higher overall value, so long as the real estate continues to appreciate. Otherwise, selling is still generally the best financial conclusion over the short and intermediate term.

The decision to sell or maintain and lease real estate after a business sale can be complicated depending on the Seller’s financial goals, investment risk tolerances and timeframes, and post-transaction roles in the business. However, careful analysis of the above considerations and input from trusted advisors can help a Seller determine the optimal course of action for real estate in a business transaction.

© Copyright by EdgePoint, M&A advisors. You can reach us at 216-831-2430, or on the web at www.edgepoint.com

By EdgePoint

One of the least understood and used financing sources for M&A transactions is the SBA 7(a) term loan. Because of its maximum loan size of $5mm, it can be used in smaller middle-market transactions, especially individual, management and partner buyouts with companies up to $3mm in EBITDA. This type of loan is made by a bank, and is guaranteed by the SBA up to 75% against any potential losses that the bank may have on a defaulted loan. The SBA rules (also called SOPs) must be strictly followed by banks to be eligible for default reimbursement.

For those transactions that are appropriate and qualify, the terms of the loan structure are very attractive. Banks are allowed to extend up to 10 year terms, on a mortgage amortization basis (level payments) and are capped on the interest they are allowed to charge at prime plus 2.75%. There is supposed to be no minimum collateral requirement, but some banks apply arbitrary collateral standards for the transactions they are willing to enter into. For those banks that follow the SBA guidelines, no minimum collateral is required, which makes these loans especially useful for services, distribution, or high margin businesses, where there would not be a sufficient amount of collateral available to secure the loan amount.

For normal cashflow loans, most lenders that are willing to do an under-collateralized transaction under $3mm in EBITDA would require repayment terms of 3-5 years, and generally recapture excess cashflow to pay back the loan in the shortest amount of time they can. This uses precious cashflow for repayment of senior debt in the first years after a transaction, which generally could have been used more effectively for growth, working capital and any transition issues that may have come up. Instead, the bank requires the accelerated repayment of its loans, and that can stifle the growth of the business. SBA loans generally have 7-10 year repayment terms, with no cashflow recapture, allowing the business to use the cashflow for those more important reasons.

In order to consider whether this loan program is appropriate for any transaction, certain pre-requisites apply. First, this is a personally guaranteed loan, which would prohibit most funded private equity groups from using this loan structure. Individuals or investor groups willing to guarantee the loans are required in order for the bank to make this type of a loan. In fact, any investor that owns 20% or more of the equity post-transaction is required to sign personally jointly and severally for the full amount of the loan. Many buyers misunderstand and believe that they have to have the amount of guaranteed loan available to the bank to collect, which is not true. The bank is required by the SBA to get the guarantees to comply with the loan guarantee program, but it is not necessary to actually have any particular net worth to qualify for the loan.

The second consideration is the type of transaction that is being proposed. There are certain rules that need to be followed according to the SBA SOPs. Some of those rules are below:

Another consideration for 7(a) loans is the equity contribution. For any loan that is not fully collateralized, and the company has more than $500k of goodwill (which will be most lower middle market transactions), the SBA requires that there be 25% “equity” in the transaction. That equity can be made up of existing equity (partner buyout), cash and/or seller notes that are deferred for two years, with no payments of interest or principal until the third year, and then can be paid as agreed. Most banks will require at least 10% cash or existing equity for acquisition transactions, but the remaining amount can be in the form of a deferred seller note. This gives a great deal of leverage to the buyer with essentially 9x leverage on equity, with 10 year terms for a senior bank loan and seller notes.

The credit test for the banks that follow the SBA guidelines is that the deal must cashflow to a 1.15x fixed charge coverage, meaning that the EBITDA needs to be 1.15x the Principal, Interest, Taxes, and Unfunded Capex, and the SBA considers that to be sufficient cashflow to make the loan. On a 10 year, low interest rate loan, this generally accommodates between 3-4x EBITDA comfortably against this test. Some banks will require higher financial ratio tests, or cap the loans at a senior debt multiple, but generally those caps are still much better than what you would get at a traditional cashflow lender and at lower interest rates.

Some advisors and buyers erroneously believe that the fees are too expensive to make the SBA loan worth it. Loan fees for the SBA are a graduated percentage that goes up to 3% as a loan closing fee that is paid to the SBA. Even on a $5mm loan, with a higher than actual full 3% fee ($150k), the cashflow savings in the first year assuming a 10 year loan term rather than a 5 year term is almost $500k. The interest savings from a lower rate versus a cashflow lender is probably a breakeven in 1-3 years, and easy to justify over the term of the loan. SBA loan fees should be irrelevant when considering this structure as they pay for themselves many times over.

Unfortunately, most small business banker lenders don’t fully understand the SBA rules, especially when it comes to acquisition transactions. Most middle market lenders never use this tool. Further, most banks make additional rules and credit standards which are more limiting than the SBA actual guidelines of the transaction structures they would support. This is partly because if the bank doesn’t follow the SBA SOPs, the government will decline to honor the guarantee, and the bank is facing a large loss that wasn’t anticipated when they made the uncollateralized loan in the first place.

EdgePoint has worked with banks across the country to develop transaction and loan structures that comply with the SBA guidelines and have formed relationships with the banks that do these types of deals. Knowing who to go to, what to ask for, and how to follow the SBA SOP rules have allowed us to close numerous transactions for our clients using this incredibly effective but highly misunderstood financing tool.

© Copyrighted by EdgePoint. Tom Zucker can be reached at 216-342-5858 or at tzucker@edgepoint.com