Cleveland, Ohio; June 2, 2016 – EdgePoint, a boutique investment banking firm located in Beachwood, Ohio, is pleased to announce the addition of Matthew Keefe. Matt joins EdgePoint as Managing Director. In this role, Matt will be responsible for advising the firm’s clients in matters related to mergers, acquisitions, and financing transactions.

Prior to joining EdgePoint, Matt served on the corporate management team of ERICO International, a privately held manufacturer. During his tenure at ERICO, Matt held the roles of Treasurer, Director of M&A, Director of Customer Service, and Director of Commercial Operations. Before joining ERICO, Matt was an investment banker serving in various capacities at KeyBanc Capital Markets, Bruml Capital and Key Corporate Capital.

“We are excited to welcome Matt Keefe to the firm. Matt brings 15 years of investment banking experience and a strong track record in executing middle market leveraged financings, buyouts, and mergers.” said Tom Zucker, President and Founder of EdgePoint.

Matt Keefe earned his BA from Miami University and his MBA from the CWRU’s Weatherhead School of Management.

EdgePoint specializes in advising middle market businesses and owners regarding mergers, acquisitions, management buyouts, and corporate divestitures.

EdgePoint is a registered broker dealer and a member of FINRA.

Life sneaks up on you when you’re not looking. It’s called experience.

When you reflect on how it was years ago, it is clear how much the world of middle market M&A has changed – for business owners and advisors. The art of the smaller deal as we know it is quite young.

No one should want to go back to ‘the good old days’.

The Way It Was – In 1976, the market for businesses with revenues between, say, $10 million and $100 million was inefficient and very thin. Such businesses were truly illiquid assets.

Pricing of a profitable, low-growth manufacturing business, for example, was likely to be less than net book value on the balance sheet. Terms usually included a large measure of seller financing as notes or an earn-out.

An owner had the rather stark choice of selling to someone with ‘no money’ and financing the transaction himself, or possibly being acquired by a competitor likely to erase the company’s identity.

Advisors facilitating a sale of a small business then were mostly lawyers, CPAs and business brokers. In the 1970s, several of the Big Eight accounting firms (now Final Four?) began to introduce clients who wanted to buy to clients who wanted to sell, but there was dynamic tension between the Independence principle and entrepreneurial investment banking practices, such as contingent fees and client advocacy.

Private Equity Is Born – In the 1970s, Nick Wallner, PhD, an entrepreneur who acquired a small business using a debt-based technique borrowed from the commercial real estate industry, published a thick soft cover tome with the catchy title How To Do ALeveraged Buyout or Acquisition. The Leveraged Buy Out, or LBO, was born and the world changed. I spoke on LBOs in London in 1980, and the audience was largely barristers and chartered accountants eager to understand the new transaction they had heard about – revamping the right hand side of the balance sheet from mostly equity to mostly debt. The hot topic earned our seminar a mention in The Financial Times.

The underlying theory is that Investment Risk (of the private equity firm) equals Business Risk (the stability of the operating company) plus Financing Risk (debt). The more consistent the operating company’s cash flows, the more debt the investment can handle, and vice versa.

With the low pricing parameters mentioned above and ample assets as collateral, a buyer needed very little equity (maybe 5% of the purchase price) to finance an acquisition. The operating plan after closing was simply to use the company’s cash flows to pay down debt, selling in five years in another LBO.

Soon entrepreneurial buyers began to seek suitable ‘boring’ businesses and, if needed, pass the hat to their friends, deal by deal, to provide the needed equity. Voila! The owner could receive cash at closing and the business remained independent.

Private equity was not a glamorous business in its early days. I remember meeting with the pioneer firm Kohlberg Kravis Roberts & Co. in its mid-town Manhattan offices, which were definitely underwhelming. They had raised a first fund of $31 million in 1977 to fund a number of smallish acquisitions. But soon, KKR left the middle market for loftier transactions, and in 2000 acquired RJR Nabisco, as chronicled in Barbarians at the Gate.

With competition, of course, valuation multiples for suitable businesses began to rise, and private equity firms had to hone a distinctive strategy to find a competitive edge. Many began to differentiate themselves. For example, Wingate partners sought ‘buy and fix’ situations, and other financiers began to work with experienced operating executives having deep operating experience in niche target markets. Riverside opened offices on four continents to help portfolio companies, and add foreign companies to their portfolio. The concept of bringing more to the table than money was born of necessity.

Another result of rising prices was the need to grow the business, organically or by add-on acquisitions, to achieve higher earnings and a possible multiple expansion, to hit target investor returns.

Private equity firms’ interest in diverse targets, and more financing options, meant that other types of businesses, like distribution, transportation and services, saw a wider range of financial suitors.

Recently, with interest rates on fixed income investments at historic lows and stock market multiples sometimes frothy, family offices have added direct acquisitions of private companies to their portfolio mix, to boost overall returns. Usually, they buy and hold a business, making them an attractive alternative in the eyes of many company owners concerned about a ‘quick flip’ by a private equity firm.

A Place For Mezzanine Financing – As richer acquisition multiples became commonplace, the need increased for nuanced financing structures to make acquirers’ financial return models work.

Banks’ willingness to lend senior debt (least costly financing) into a “highly leveraged transaction” (as defined by the Comptroller of the Currency, The Federal Reserve Bank and the FDIC) is limited by concerns of a recession, rising interest rates, a company’s track record and regulatory pressures.

Accordingly, in the 1980s insurance companies, savings and loan associations and eventually limited partnerships formed available pools of risk capital, such as subordinated notes and preferred stock, with characteristics straddling debt and equity. ‘Mezz’, as it is affectionately called, is midway between senior debt and equity in cost and rights.

Mezzanine lenders earn their returns as a combination of cash interest (fixed or floating with a base rate), PIK interest (accrued but not paid until repayment is due) and ownership rights (e.g. attached warrants).

The ESOP Evangelist – Louis Kelso, a visionary economist and merchant banker (Kelso & Company) who thought everyone should own a piece of the action, invented the Employee Stock Ownership Plan, a unique device for selling a company to all or most of its employees. Kelso created the ESOP in 1956 to enable the employees of Peninsula Newspapers, a closely held newspaper chain in the State of Washington, to buy out its retiring owners.

For years, Kelso worked with Senate Finance Committee Chairman Russell Long, to build into the 1974 ERISA legislation generous tax advantages for both the ESOP company and the owner who sold to an ESOP.

Sometimes misused (as in a failing steel company), the ESOP used as intended has created many millionaires on the factory floor and at steel desks. The tax carrot appeals to tax-adverse owners, and drives the use of this technique even today. I knew and presented a series of seminars with the impassioned Louis Kelso. It was a near-religious experience.

But Wait – There’s More – Reflections will continue in the next two issues of the EdgePoint Newsletter.

The Author’s Journey: It can be helpful when reading someone’s perspective to understand his or her professional experience. Here is mine.

With an engineering degree, a fresh MBA and a stint as Private in the U. S. Army (a reality check if there ever was one), I settled in at Ernst (before Young), auditing a rainbow of mostly mid-size companies and learning about businesses and industries from the inside out. In the mid-1970s, I joined the firm’s nascent merger and acquisition practice when the M&A market was robust and we were still figuring out where and how to play. Eventually, I led U. S. Merger and Acquisition Services for 10 years.

It was stimulating and educational, with client engagements from Hollywood, CA (for Sammy Davis Jr.) to Jamestown, NY (selling a Tier 1 supplier to Chrysler and Volvo). There was a lot of international travel. A capstone engagement (and digression) for me was an on-site study of how to improve venture capital access in Indonesia, Thailand, Malaysia, Pakistan and Sri Lanka, conducted for the Asian Development Bank, a large non-governmental organization. Results included funding for three start-up venture capital firms and the passage of recommended legislation by Thailand.

Months later, Ernst & Whinney moved its headquarters to New York, and I founded The TransAction Group, a boutique M&A firm serving middle market businesses. With a former Ernst colleague, we ran and grew the firm. We closed 75 transactions, nineteen of them cross-border. In 2008, we sold to EdgePoint, a dynamic young firm with shared values and the same mission: to bring top quality professional M&A services to owners of smaller businesses. I was happy to trade my former administrative duties for the role of Managing Director, developing business and serving clients.

Tom Cruise uttered the famous line, “Show Me the Money!” when portraying a sports agent in the 1996 movie “Jerry Maguire”. His client (played by Cuba Gooding Jr.) was urging Tom’s character to focus on maximizing the cash compensation in his contract. It was clear that “the Money” was the only aspect of his contract negotiations that was important to him.

As investment bankers who have closed 300+ transactions over the last 40 years, we have learned that successful deals are rarely just about “The Money”. All of our clients have unique criteria for a successful sale and it is our job to balance the client’s qualitative factors throughout a sale process.

Two recent experiences highlight this observation.

We represented a business owner that was 50 years old at the time, unmarried, and had a desire to pursue interests outside of the business. He did not need the proceeds to retire comfortably.

We conducted a sale process that produced 20 offers with 6 premium offers relative to his target selling price. After meeting with the premium buyers, one submitted an offer well above the other bidders. Despite the significant potential financial gain, our client was hesitant to accept. He indicated to us that he preferred one of the lower bidders. During the process he came to realize that his key employees had grown to become “like family” and he felt the highest bidder would not be the best steward of the business going forward. With that understanding, we were able to negotiate an acceptable albeit lower value with another bidder that would allow the key employees to be protected post-transaction.

Another engagement involved a second-generation business that did not have a clear successor. The business was the largest employer in the town where they operated. Our clients had significant wealth accumulated from their years of operation.

During our sale process the owners were concerned with maximizing value to further fund a number of charitable organizations they supported. Additionally, the owners desired a buyer that would commit to maintaining the existing facility and employees. Our process proceeded accordingly and resulted in a sale to a buyer who shared the same vision for the business – and community – as the seller. The sellers traded maximum proceeds for the assurance that the business, employees and community would benefit long term.

Much like the Jerry Maguire character, an investment banking partner must explore and understand the core needs and desires of their clients to determine the qualitative factors (i.e. stewardship, legacy, employees, community) that can also influence the quantitative ones (i.e. personal wealth accumulation, retirement planning, generational wealth). When these attributes are identified and properly communicated to buyers, the transaction becomes much more than just, “Show me the money!”

By design, merger transactions can have significant strategic value to two parties with different yet complementary operating models and philosophies. While these operating and cultural differences can yield a stronger and more complete organization, they can also make for a difficult transaction process—which in turn may put at risk the great strategic potential contemplated by the combination in the first place. This article illustrates this common transactional phenomenon and proposes several techniques to ensure that tension inherent in opposing but complementary business philosophies does not prevent a stronger combined entity.

Consider the following fact pattern:

Company A, a small but growing engineering firm, achieves great success in the industrial sector as it provides the same sophisticated services offered by the largest engineering firms in the world, but with client responsiveness and agility common in smaller firms. This responsiveness and agility, combined with some entrepreneurial risk-taking, contributes to better profitability. At the same time, Company A needs a succession plan, deeper operational resources, and the resources of a large engineering firm to continue to support its growth. Company B is a $1 billion international firm with depth and sophistication of resources to support growth. Overly conservative because of adherence to strict operational processes, Company B is laden by bureaucracy and lack of responsiveness. While possessing deep marketing and other operational resources, the organization is too heavy and sluggish to penetrate the fast-growing industrial sector. Furthermore, layers of oversight and conservative decision-making contribute to limited risk taking—and lower profitability.

Like all successful merger transactions, Company A and B realize they can both benefit from becoming one. The merger gives Company A the scale and international access needed to continue its growth. For Company B, the merger introduces a culture of vibrancy and entrepreneurship that contributes to far greater profitability on its core business. However, in classic “Catch 22” fashion, the same factors that make the transaction such a synergistic fit and success make it more difficult to execute from a transaction perspective. The exact characteristics that each needs in the other turn out to be those that cause trouble during diligence and legal documentation. Company A is concerned that greater recordkeeping and other administrative burdens from integration into Company B will impair the flexibility that makes it successful and profitable; likewise, Company B is concerned that it will be unable to keep up with the more agile and entrepreneurial Company A and is uncomfortable with some of its historical risk profile. And both parties—relying upon their historical culture—are emboldened in their transactional positions, while acknowledging they need the other’s culture to survive and grow in the future.

So how can two very different parties that need each other so much ensure that the fantastic transaction benefits are not lost to cultural differences? While it’s easy to say that both parties need to understand the other’s perspective, seasoned transaction professionals know this is easier said than done, particularly in the heat of transaction negotiation. While there is no foolproof plan to ensure a transaction stays on track in this situation, a few tactics can be employed to prevent the Catch 22 from destroying a potentially perfect combination.

Establish Early Integration Expectations of Both Parties — While most early transactional negotiations do contemplate high-level integration analysis, most often this topic is deferred until much later in the process. In addition to discussions about value and strategic potential early in the transaction process, both parties should not be bashful about using early conversations as a forum to explore integration specifics. Planned reporting hierarchy, extent of decision-making, level of financial and other business-management reporting, and the risk-management processes and policies of the respective parties are good topics to consider before the parties decide to negotiate on an exclusive basis. For Sellers running an auction process, requesting the Buyer universe to document early their expectations for these integration items, while the Seller has leverage in the transaction, is ideal. If a Buyer is unable to document how they will take into account the unique aspects of the acquired business, it might mean that the buyer is unable to appreciate a different business model.

Remember Strategic Fit — During due diligence and document negotiation, the cultural differences of both parties become very evident. For example, a smaller company’s lack of formality in documentation may cause hairs to rise on a larger more corporate buyer; similarly, a large strategic organization’s diligence level and detail may come across as overly burdensome to a smaller Seller and may be perceived as a preview of the hassle associated with integration. To prevent this from causing the transaction to derail, a “check-in” during diligence, in which both parties meet to reconfirm strategic fit, may be needed to ease tensions around the cultural differences and reassure both parties.

On-Site Buyer Visits — A common tactic to alleviate Seller’s concern about oppressive post-transaction management is on-site visits to the buyer. Most of the diligence and negotiation process is at Seller’s site. This one-sided investigation can certainly contribute to a Seller’s integration anxiety. Scheduled on-site visits to the buyer, where Seller can actually view the processes in place, are very effective to promote good feelings about synergy. Buyer should demonstrate some of the benefits of integration into their organization, such as access to a very large Human Resources and Marketing Department, for example. Allowing buyer to see the benefits of integration, in the middle of sometimes tense negotiations, is an excellent way to solve problems associated with cultural disconnect.

Disconnect Diligence from Operations — It is common for a Seller to associate the due diligence process with post-transaction life. As a result of the diligence investigation, Sellers often envision long interrogation and oppressive recordkeeping as part of life with the Buyer. It is important for a buyer to disassociate diligence from integration, understanding that the Buyer has an unpleasant job to do before both parties can realize the great benefits of combination.

The cultural differences that often come with the greatest strategic fits can be exacerbated by transaction-process functions. When parties can work through cultural differences during this process, the potential for a promising partnership is assured.

Rarely am I able to suggest that anyone follow the example of a politician, but these unique creatures show ways that people often handle sensitive communications during an M&A process. During every campaign cycle, we observe numerous candidates perfecting the time-tested techniques of denying and deflecting challenging questions. Although I despise politicians’ verbal maneuvering and lack of transparency, I respect how they achieve their main objective of preventing discussion of a topic that they want to avoid. With this background, below I consider several methods that people use to handle the most sacred truth…my company is for sale!

Deny

“I have no idea where they would have gotten that idea”, “Just rumors”, and “My company is not for sale”, are just a few of the common responses that an owner will use to deny the fact that indeed, their company is for sale. The outright denial is a common technique to refute the rumors. A denial might be appropriate where an owner is legally bound by a Confidentiality Agreement with a buyer (e.g., a publicly traded buyer) not to disclose that a transaction is in process. This approach often does not feel consistent with the character of the owner, but certainly would make a politician proud.

Deflect

Typically, early in a sale process, the business owner will deflect questions and observations. Recently, the V.P. of Marketing for a client of ours approached the business owner with the comment, “I recently heard from a supplier that our company is on the market”. Despite the efforts of a skilled investment banker using code names, Confidentiality Agreements, only contacting senior level executives, and demanding a very tight timeline, occasionally someone in this chain of communication will breach confidentiality regarding the deal. Our client was disappointed in the realization of a breach, but was forced to respond quickly. He confidently responded to the executive, “Everything in life is for sale at the right price.” In this example, the deflection seems to have satisfied the V.P., but there is no certainty that the owner’s answer completely dismissed the V.P.’s lingering concerns (or those of others involved).

Disclose

Many business owners utilize some of the previous approaches in the early stages of the sale process and then eventually disclose the sale prior to Closing. The later in the process that an owner can disclose the fact a sale is likely to occur, the less likely it is that employees, competitors, or other parties not directly involved in the negotiations will influence the outcome. Typically, an owner will notify a few key managers early in the process to provide proper insight and support, and then expand the number of internal people aware of the pending event as buyer interest and offers solidify. The disclosure to customers, other employees and family members is often deferred until just days or weeks prior to the closing of the sale. An owner must resist the desire to share the good news and defer disclosing until they are ready to handle the barrage of inquiries, questions and concerns and the deal has sufficiently solidified. As one would expect, it is often those with less facts and control that will worry the most and often extend their anxiety and uncertainty to others who would be impacted by the sale. It is human nature to fear uncertainty and circumstances beyond one’s control.

In order be prepared for questions about the sale before you have raised the issue, an owner should work with their investment banker to be prepared. Developing a communication plan at the start of an engagement is critical. The owner should have a truthful answer prepared for various inquiries, depending upon who raises the issue (i.e. employees, customers, suppliers). The answer may be slightly different for each or perhaps a consistent answer will be needed- each deal is different. It does not happen often, but being confidently prepared to answer the question of whether a company is for sale can be rehearsed and to properly address the inquiry.

In business, as in life, communication can be everything. During the sale process, this statement is even more evident and true. The intensity of emotions that a business owner has as he or she begins to think about selling “their baby” is very high. The key managers anxiously observe private conversations and unusual requests while thinking to themselves about the security of their job. The advisors (i.e., attorneys, accountants and bankers) strive to protect and advise long-time clients, but they are also motivated to preserve their future business with their client. It is in this environment that a skilled investment banker works, and why deal communications are so critical to a successful transaction. Preparation of a communication plan for this process may not qualify a client to run for political office, but will certainly give them comfort that they are answering with integrity in a manner that does not jeopardize the success of the sale.

By Russ Warren, Managing Director and

Tom Zucker, President

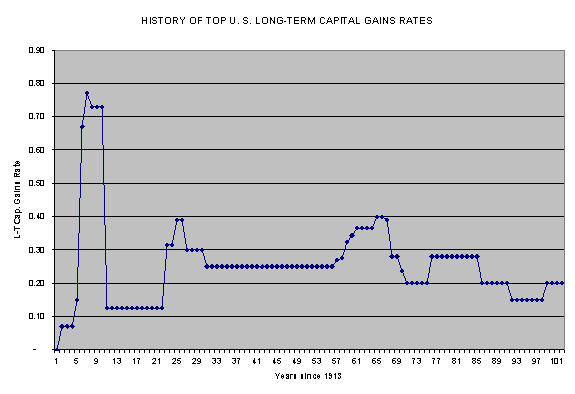

At 15%, today’s maximum long-term capital gains tax rate (LTCG) is the lowest it has been in the last 75 years (see chart below). In 2003, this rate was reduced to 15% from 20%, with a sunset provision, and is effective through 2010.

If Congress and the Administration were to do nothing, the LTCG rate would go back to 20% on January 1, 2011.

However, with bailouts, stimuli packages and new social programs collectively costing trillions to fund somehow, what better place in Washington’s view to raise revenue than from capital gains? There is also historical precedent. As recently as 1996, the LTCG rate was 28%. Throughout the 1970s, the rate was 28% to 40%.

The prospect of paying more to Uncle Sam if you close the sale of all or part of your business after December 31, 2010 is starting to get on owners’ radar screens. The impact on an owner’s wallet is shown by the following hypothetical example.

If a business owner obtains $10 million more in proceeds (that qualify as long-term capital gains) than his or her tax basis, the LTCG tax at 15% would be $1.5 million. However, if the LTCG rate were raised to 30%, the extra $1.5 million tax bite would reduce take-home proceeds from $8.5 million to $7 million, an 18% reduction.

In other words, to realize $8.5 million in ‘take home’ proceeds at a constant pricing multiple, the business would have to generate a significantly higher EBITDA. As shown below, for each 10 percentage point increase in the LTCG rate, a business would need to generate 13% to 15% more in Earnings Before Interest, Taxes, Depreciation and Amortization.

LTCG Rate

Req’d EBITDA

Assumed Multiple

Req’d Proceeds

Keep Factor

Take Home

15%

2,000

5

10,100

85%

8,500

20%

2,125

5

10,625

80%

8,500

25%

2,267

5

11,333

75%

8,500

30%

2,429

5

12,143

70%

8,500

35%

2,615

5

13,077

65%

8,500

So Uncle Sam is having a limited-term offer – a 15% capital Gains Tax. But to take advantage of this offer, time is of the essence. The typical sale of a middle market business – to an unrelated party, an ESOP or management – requires six to twelve months (depending on factors often beyond the seller team’s control) from the time a financial advisor like EdgePoint is engaged. So, to close a transaction by December 31, 2010, planning and discussions should begin as soon as possible. In the world of Taxes, ‘almost getting it closed by the deadline’ doesn’t count, and could cost a lot of money.

We would be glad to discuss your situation in complete privacy, and assess the best time to begin, given your company’s recent performance and outlook.

After working decades to develop your business and career, you finally arrive at the decision to sell the business. You’ve done a fantastic job identifying the buyer and negotiating the price and other sale terms. You’re relieved and satisfied, and can see the “closing” within a short 90 days, and the approaching transition to what comes next.

But, then something happens – the transaction falters, stalls, grows apart. You’re left wondering, “what happened?”

After closing hundreds of transactions, we understand that transactions can derail for many reasons. However, we’ve observed a consistent series of reasons that dominate the question “why do deals not close?”

Reason 1: Lack of Financing – The most common reason deals stall is a failure to arrange suitable financing. Financing is the life blood of every deal. Over two-thirds of a transaction’s purchase price is commonly financed in some way – bank financing, subordinated debt, seller financing, or junior equity.

Many seller’s expect that the buyer of their business is skilled and knowledge in the art of financing a business. Quite often this is a very dangerous assumption. In fact, many buyers of closely held companies do not have strong financing experience. The seller or their investment banker must take a proactive role in assisting the buyer in securing the necessary capital. The seller’s advisor should be able to confirm that the buyer is dealing with the right type of lenders and that the lenders have the required information to quickly get funding approval.

Reason 2: Emotions Run High – The second most common reason business sale transactions stall is out-of-check emotions. Selling a business is a highly emotional event; it involves many issues, and much uncertainty, stress, and family pressures. It bears on many aspects of the owners’ lives. From the joy of expecting a multi-million dollar payoff, to the thought of leaving trusted 30-year employees, emotions can be intense, and parties are on edge.

During the sale process, your ability to check emotions at the door and allow your advisors to guide you through the transaction can be critical to success. Know that while what the Buyer and his advisors say or do may at times infuriate you, it’s in your best interest to permit your skilled advisor to insulate you from emotional issues. Be smart, defer to your advisor’s experience rather than just “reacting.”

Reason 3: Ongoing Business Performance – The process of closing the sale of one’s business brings new distractions and requests for your already scarce time. The buyer’s request for documents, endless questions about your business, meetings with advisors, negotiations, and many multi-party dealings all but evaporate any time for running your business. In addition, it is hard for a departing owner to remain focused on the business when visions of their future with more personal capital and time flash in front of them. Unfortunately, it is at this time that your business is most in need of your leadership and focus.

In order to survive the closing process, it is critical that you have an experienced and disciplined team comprised of your investment banker, lawyer and accountant to deflect much of the distractions as possible. These advisors can enable you and your team to remain focused on keeping your business on track. If Sellers fail in this regard, buyers get nervous, have reason to renegotiate valuations, get concerned about customers leaving, and can become apprehensive about closing the transaction.

Reason 4: Creeping Greed – The allure of money is only intensified by the opportunity for more money. As the process of selling your business advances, owners and advisors will work to secure the best deal and terms possible. During this process many owners and their advisors become filled with more greed. While Gordon Gecko from the famed movie Wall Street will tell you that “Greed is good”, it is our experience that “too much greed kills deals!”

It is important for the owner to remain in control of the deal and to ensure a principled approach to the final negotiations. Often over-zealous advisors will attempt to prove their value to a deal and their client by over negotiating documents or non-essential deal points. When millions of dollars are on the table, this over negotiation often breeds distrust, discomfort, and annoyance among the parties. In addition to the distrust, the process of over negotiating often costs the deal by losing essential deal momentum. It’s very, very important to keep the greed, the emotions, and the posturing of negotiations in balance with the parties’ end objectives, which includes getting to closing with reasonable levels of certainty and risk.

Reason 5: Lack of Accessible and Reliable Answers – The last, but definitely not least, reason deals crash is seller’s failure to quickly respond with clear answers to buyer’s questions. If a buyer has to struggle to find answers to relevant questions, it becomes a challenge for the buyer to pay the offered purchase price. We call this “getting the house in order.” It’s absolutely critical that legal and accounting documents and other supporting materials are in place and at hand well in advance of the closing process. The agreed time frame between sale agreement and closing date should not be a period of forced “discovery,” but one of simple “confirmation.”

All information must be prepared and organized into a very clear and consistent data package and made available electronically or in hard copy so that the buyer’s due diligence team can quickly and easily access it for answers to routine and relevant questions.

While there are many reasons that a sale of business does not consummate, the lack of credible information, greed, unchecked emotions, lack of financing and a drop in your business performance are the most common reasons for a failed deal. It’s one thing to get an offer to buy your business; it’s another thing to close a transaction in the midst of emotions and greed, customer’s movements, and overall business risks. The job of a skilled intermediary is to navigate these issues and guide the seller to the transaction closing they’ve worked their entire life for.

Business owners should consider an Employee Stock Ownership Plan (ESOP) when their management team is capable of running the business without the selling shareholders (or can adeptly replace the owner/manager) and the company doesn’t face imminent distress.

After a company’s sale to an ESOP and the eventual retirement (exit) of majority shareholders, the management team usually operates the business. In many cases, members of management may also be the ESOP’s trustee. In either case, management is running the business as if they purchased the company. If current management is not capable of running the business without the departing shareholders, then suitable management replacements must be found or the Company and ESOP risk failure.

EdgePoint often describes ESOPs as a “tax-advantaged management buyout.” Because management runs the business, and are often the highest paid, they have a larger share of ESOP share allocations. As owners, management benefits from their own success—this can be an effective motivator for the team. Tax advantages ranging from deduction of principal on ESOP formation debt to the complete elimination of income tax for 100 percent ESOP owned S-Corps create a tailwind for these transactions, helping ensure success as management assumes control of the business. There are plenty of other nonfinancial reasons to consider an ESOP, but the tax benefits can be compelling.

Other parameters to consider include the size and health of the company, the age of its workforce, and its debt capacity. Almost any size company can afford an ESOP, contrary to the common “minimum-size” myth. Costs to administer an ESOP are very similar to those of a 401(k), and most companies can afford the third-party administrator (TPA) that manages the 401(k)’s retirement trust accounts. The primary difference with an ESOP is that every year the company must secure a certified valuation of the shares to determine their value to participants and establish the buyout price for new share offerings or terminations/retirement redemptions. Valuations can cost from $5,000 to $25,000 for most companies per year, which is usually not prohibitive. Outside trustees, bank financing, attorneys and consultants are additional and often optional costs, but the primary annual ESOP administration costs are the TPA and annual valuation.

Workforce age matters merely because of repurchase-liability planning, but is not necessarily prohibitive. If a workforce is mostly older, the Company faces repurchase obligations earlier. This may trigger a liquidity need. However, flexible options exist that can be built into the ESOP plan, such as deferring repurchase payments while the ESOP formation debt is serviced, delaying the start of payments to participants and regulating the stream of those payments. Additionally, if an older workforce starts to retire within a few years after ESOP formation, not all of the stock will be allocated by then, and the company has had less time to grow its valuation. This slows share redemption, and redemptions are for less value than if the shares had been there longer.

Debt capacity is important to a new ESOP for two primary reasons. First, because no “equity” is infused by shareholders to purchase the shares, debt is the only funding source. Second, debt is used for liquidity to operate the business and eventually repurchase shares from ESOP participants. If the Company has limited borrowing ability, it makes ESOP a less viable alternative. Alternatively, the benefits to financing an ESOP is that higher tax advantages allow lenders to lend more money into an ESOP due to the business’ higher cash flow, and personal guarantees are generally not necessary. Certain government loan programs and mezzanine lenders have special lending rules that promote financing ESOP transactions.

If you are contemplating transition, and your management team is capable of running the business, regardless of whether you think they “have the money” to buy you out, contact us. We have financed management teams for both management buyouts (MBOs) and ESOPs with little or no equity.

By Russ Warren, EdgePoint and Lori Siwik, SandRun Risk

The Role of Divestitures in Profitable Growth

Strategy is as much about what you do not do as it is about what you do, says Harvard’s Michael Porter in his classic Harvard Business Review article, “What is Strategy?”

“Leading companies view divestments as a fundamental part of their capital strategy” concluded Big 4 accounting firm EY in itsGlobal Corporate Divestment Study 2015. EY also found that nearly three quarters of the firms studied are using divestitures to fund growth and two thirds achieved a higher valuation multiple after divestment.

As a company grows and evolves in a changing environment, and as it makes significant acquisitions, some business units no longer fit well or perform well and may be worth more to others, while the divestiture proceeds can be redeployed profitably in the core business. That’s when less is more.

A pruning exercise, or corporate divestiture, can create significant value for shareholders as well as increase opportunity for unit employees and other stakeholders.

The Board and C-Suite executives responsible for a divestiture may need to be as concerned about managing risks and protecting the company’s reputation with key constituencies as they are with purchase price. This article addresses both concerns.

Two keys to creating maximum value with minimum risk when divesting a business unit are: 1) adequate planning and 2) professional execution. These tasks may require specialized resources from outside the company.

The Divestiture Process

The divestiture process begins with reviewing operating results and growth plans, and raising questions about the future role of each business unit.

If a company decides to divest, a divestiture team must be assembled to begin planning the project. When the project is initiated, execution will fall into two types of tasks: managing the unit to be divested and managing the divestiture process itself.

The Divestiture Team

In a large company, the corporate development department often manages the divestiture process, and may engage and oversee an M&A advisory firm to handle most activities. In a smaller company, the chief financial officer typically leads the project, with outside advisors.

A financial executive is often assigned to verify the numbers that will be presented to a buyer, adjust unit financial statements to a pro-forma stand-alone basis and, at closing, “unhook” the unit from the company’s IT systems or arrange transitional services for the buyer.

Raising The Question

Whether part of a periodic review of unit performance or a larger corporate strategic decision, the divestiture process begins with raising The Question: ‘Should this unit be divested?’ – and a number of related questions, such as:

Does this business unit have strategic value in the company’s future?

What are the value drivers for the unit? For example:

Intellectual property, proprietary products, services or skills

Customer base, access

Skilled management team

Would the unit be more valuable to another owner? What kind of buyer?

What financial effects would divestiture have on the remaining business?

Unabsorbed overhead

Reduced design capabilities

Loss of inter-divisional sales

How can any negative effects be prevented or minimized?

Sale of idle facilities

Outsourcing

Long-term supply agreement with the buyer as part of the deal

The Decision

The recommendation to divest is usually made by the operating executive above the unit, but the decision is often made by the CEO, after appropriate involvement by other senior executives and the Board of Directors due to sensitivity to the impact of the divestiture on employee morale and strategy.

A decision of a public company to divest may have less emotion than the decision by a private company owner to sell his or her business, but it can be difficult nevertheless. Non-price considerations, like loss of jobs in the local community, risk of shared brand names, and environmental stewardship may be very important to the divesting company’s reputation. In smaller divestitures, price may be overshadowed by these concerns to protect the company’s reputation.

If the decision to divest is made, a second set of questions is raised:

What type of transaction would fetch the highest price and best terms?

Sale to strategic acquirer

Sale to international strategic acquirer

Management buyout with private equity sponsor

Partial sale to a private equity group and management

Employee Stock Ownership Plan leveraged buyout

Spin-off/Initial Public Offering

Liquidation/shut-down

Do we want a long-term supply agreement with the unit?

When is the best time to begin the divestiture process for this unit?

Industry and macro-economic conditions

Unit-specific situation

‘Fix-up’ activities needed to maximize value

How will we manage the unit until it is sold?

How will we execute the divestiture process?

Pre-emptive Due Diligence and Planning

Before contacting buyers, management (with the support of financial and legal advisors, and other consultants) should identify and address potential issues that would concern a buyer. The benefits of thoughtful planning and resolving risks up front include:

Increasing the likelihood of a timely, successful process.

Presenting more accurate and reliable financial information in the divestiture marketing materials

Identifying and documenting adjustments with positive financial impact (rather than reacting to a purchaser’s negative adjustments).

Strengthening negotiating position on risks at the beginning of the transaction

Preparing the management team for likely questions by potential purchasers.

Minimizing disruptions to ongoing business and management.

A careful review of the unit to be divested should be undertaken. That review should include:

Predictability of future revenues; market conditions and trends; any issues with key customers

Financial records and results, including detail accounting records, systems and budgets

Infrastructure and operations – supply chain/raw materials, products, hazards, and technology

Environmental and regulatory compliance

Employee policies and agreements; healthcare issues

Contracts – review for risk transfer provisions that may have promised indemnification or conferred additional insured status on the seller’s suppliers, customers, or past or present corporate affiliates.

Current risk management/insurance program

To maximize value and minimize risk, it is important to protect against liability exposure, so the planned due diligence should include:

Insurance[*]– organizing in a database all historic insurance policies, applications, schedules of insurance, claims data, insured and uninsured liabilities, corporate history, and a summary of losses by line of insurance. The insurance program should be reviewed to determine: (1) there are no gaps in coverage; (2) there are adequate limits; (3) there are no notices of cancellation; (4) whether the policies are ‘claims made’ or ‘occurrence based’; (5) whether there are high deductible, fronted policies, or retrospective premium programs; (6) if there are exhausted policy limits; (7) if there are any open or pending notices of claims to insurance carriers; (8) if any of the policies require an extended reporting period; (10) if there are any weak insurance carriers on the historic insurance program; and (11) if there are any “change-in-control” provisions in the insurance policies that either restrict coverage or eliminate coverage with a change in ownership.

Environmental and pollution liability– ensuring that all information regarding Phase I, EPA inspections, past use of property and disposal activity documentation is available.

Property appraisals– gathering documentation for all property to be transferred

Overall risks– identifying risks and establishing that those risks have been adequately addressed and covered; consider reps & warranties insurance for matters of concern to a buyer.

Locating, reviewing and organizing corporate records– articles of incorporation, by-laws, corporate minute books, and stock transfer records

A virtual data room (VDR) can expedite closing by making the due diligence documents easily available on-line and provide appropriate security and monitoring capabilities. The cost of this service for mid-size transactions has dropped considerably in the last several years.

Managing the Unit Being Divested

Management of the unit being divested focuses on enhancement of its attractiveness and selling price. Focus is on unit profitability. Inventories and receivables are managed aggressively. Capital expenditure requests are reviewed carefully, but not necessarily turned down.

People, too, are important assets, and communicating with employees and key customers – both the message and timing – deserves careful attention. Some companies develop a detailed written ‘announcement plan’. Non-compete agreements, ‘stay’ packages, and other means to secure the cooperation of key unit personnel can be helpful.

Managing the Divestiture Process

The Divestiture Team’s job is to create the most effective form of competition for the unit among motivated, qualified buyers, although not all divestiture candidates are attractive enough to enable an auction.

Most companies offer a unit pretty much ‘as is’. They often are, however, willing to warrant the big items, and take seller notes as part of the consideration when necessary to close.

Finding the best buyer candidates and structuring the transaction creatively are skills necessary for a successful divestiture. There are a number of buyers that specialize in acquiring divested businesses, as well as logical strategic acquirers and private equity firms with interest in the relevant sector.

With the range of possible transaction types cited earlier and considering the size of the unit to be divested, the divestiture team may need specialized resources to handle these tasks effectively. If they are not available in-house, an M&A advisor with relevant divestiture experience can be well worth the cost.

Confidentiality will be a top priority of the Divestiture Team throughout the process. Companies typically have individuals involved in the divestiture process sign a confidentiality agreement.

Providing the right information to buyer candidates is essential in achieving the best price. The value drivers and the unit’s future financial potential under an achievable ‘stretch’ scenario must be communicated in writing and discussed by unit management. DVDs enable a buyer to ‘see’ processes and locations. Sector background is helpful where buyers may not be familiar. Giving potential buyers access to all or part of the VDR can also help move the divestiture process along.

Audited financial statements for the unit strengthen a buyer’s confidence and should be provided whenever practicable. Alternatively, if there are no stand-alone financial statements for the unit, they must be extracted from the records of the larger entity. In the case of a large company selling a small unit, this may be a time-consuming but necessary activity because if the buyer doubts the reliability of the unit’s numbers, it can impede or kill the deal.

A divestiture is an important management activity because it can increase shareholder value. It requires the right people, careful planning, creativity and attention to detail.

“The euphoria of a bull market overshadows the dull drums of a bear market” is often heard in the investing community, but how true are these words in the middle market merger and acquisition business today? The desire of business owners to sell their companies for top dollar is a given, but it is often difficult to know when the merger and acquisition market is at or near its peak.

So, how does an owner know when is the right time to sell his or her business? Unlike other arenas, in the sale of a business many factors impact the decision as to the optimal time to sell. The following is a brief overview of some of the critical factors to consider:

Industry: Every industry segment has a life cycle. The life cycle of an industry often exceeds the life cycle of the individual business models that exist within each industry. The optimal time to sell is greatly impacted by competitive market forces (e.g. China), technological advances (manufacturing technologies, internet, etc.), and end user demand (e.g. no demand for typewriters). Be a student of your industry and the money factors impacting its movement.

Interest Rates: The ability to borrow capital from banks, financing companies, mezzanine capital sources and subordinated debt sources greatly impacts a buyer’s ability to purchase a business. Throughout history the lending markets have directly impacted the activity and pricing in the M&A market. The 2009 recession is the latest reference point to the impact that the credit markets has on M&A transaction volume and pricing.

Buyer Demand: The economics of supply and demand are often the most significant force impacting the right time to sell a business. Over the past several years an abundance of buyers have created a tremendous seller’s market. This over-supply of buyers has recently been enhanced by low interest rates and low capital gains tax rates. This translates into an outstanding environment to sell a business. The abundance of qualified buyers is primarily a result of the following three factors:

Private equity funds raised an unprecedented amount of funds and have an estimated $450 billion dollars of unused capital designated for acquisitions in the near-term. A majority of this capital is approaching the stage within their funds that they must invest the money or return it to their limited partners. (Don’t count on the money being returned.)

Corporate entrepreneurs continue to emerge in record numbers. These are successful corporate veterans that have decided to try their hand at business ownership either by choice or necessity. A seller must be very diligent in reviewing these types of buyers to ensure that they have the right risk tolerance and skills to be the “right” buyer, and that they have financing.

Lower cost of capital has enabled strong companies to strategically acquire undercapitalized or underperforming companies. Such buyers are often well-versed in their industry and are actively monitoring key competitors for acquisition. These buyers are often able to pay more for a company based on their lower cost of capital, lower desired equity returns (compared with VC’s), and their ability to remove operational costs due to the synergies between the combined entities.

Current supply and demand for middle-sized businesses can best be assessed by talking with financial intermediaries that specialize in buying and selling companies like yours. Other sources that can provide insight on current demand for companies are private equity firms with investments in your industry or from chief executives operating within your industry.

Company-Specific Performance and Outlook: Many businesses experienced a strong downturn in the recent recession, shed costs, and have come through stronger and leaner. Buyers care most about the most recent years when evaluating historical performance, so a loss, say, in 2009 is no longer a drag on value. Most important is the outlook for profitable growth, and that’s where many owners err. They wait until the roller coaster approaches the top (profit /growth slows) before beginning the sale process. Consulting with and hiring professionals with the knowledge and experience in these matters can ensure you make an informed and timely decision to sell.

State of Mind: As you have probably concluded by now the process of determining the proper time to sell is complex and has many factors that impact the decision. It requires a business owner to really study his market, industry and the current capital markets. This need to increase effort and diligence towards studying ones business unfortunately comes at a time when business owners considering business transition want to pull back and slow down. Slowing down unfortunately is not an answer. Utilize professional advisors to supply perspective and needed efforts to optimize the timing of your sale.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.