Leverage Gap: Large Market Deals Delayed, but Lower Market Deals Unscathed

By Tom Zucker, President

In the high-stakes world of M&A, leverage is a powerful tool that can either make or break a deal. Its impact on large market deals (> $250 million) is unmistakable, driving monumental mergers, while its influence on lower market deals (< $250 million) has historically been more subdued.

Today, lenders are pulling out of large market deals due to interest rate hikes and fears of a recession. On the other hand, lending for lower market deals remains stable and deal activity is robust.

Understanding leverage, its effect on valuation, and the gap between lending in large market and lower market deals can help sellers and advisors properly navigate the M&A market and make informed decisions.

Leverage involves using borrowed capital to amplify potential returns. Large market deals thrive on this concept, as the infusion of substantial funds enables players to execute ambitious projects, undertake defining acquisitions, and embark on high-risk, high reward roll up strategies. In such an environment, leverage acts as a multiplier, turning substantial investments into colossal ones, and fueling exponential growth. As a result, financial institutions (banks and non-banks) and private equity firms eagerly facilitate deals, reaping the rewards of substantial appreciation of these enterprises.

However, the same leverage that propels large market deals to towering heights can also lead to devastating consequences if mismanaged. The 2008 financial crisis serves as a stark reminder of the dangers of excessive leverage. Thus, the high-stakes nature of large market deals demands prudent risk management and stringent monitoring to avoid potential calamities.

Lower market deals operate in a different universe, where the impact of leverage is more muted. These deals typically involve modest leverage and rational growth expectations. For such acquisitions, traditional financing methods and equity-based structures often suffice, and leveraging is less critical for success.

Additionally, lower market deals are oftentimes add-on acquisitions to an existing platform company owned by a private equity firm. As a result, private equity firms will elect to fund these deals through the balance sheets of their platform companies.

The rationale for this leverage gap has many reasons, but the following are the three primary factors:

Risk Assessment: One of the primary reasons banks are more cautious when lending to smaller companies in an M&A transaction is due to risk assessment. Banks and non-banks perceive lending to lower market companies as riskier, with a higher probability of default. To mitigate risk, banks may offer lower leverage rates or demand stricter collateral requirements, sometimes making it challenging for lower market companies to secure the necessary capital.

Lack of Management Depth: Banks assess the management team's experience and depth before granting loans. Typically, the depth and sophistication of management relative to leveraged finance often impacts a bank’s willingness to extend additional capital.

Regulatory Constraints: Regulatory factors also play a key role in a bank’s lending less to lower market companies in M&A transactions. Courtesy of the Dodd-Frank bill, banks have imposed stricter regulations on financial institutions after the global financial crisis, which has led to more stringent lending standards.

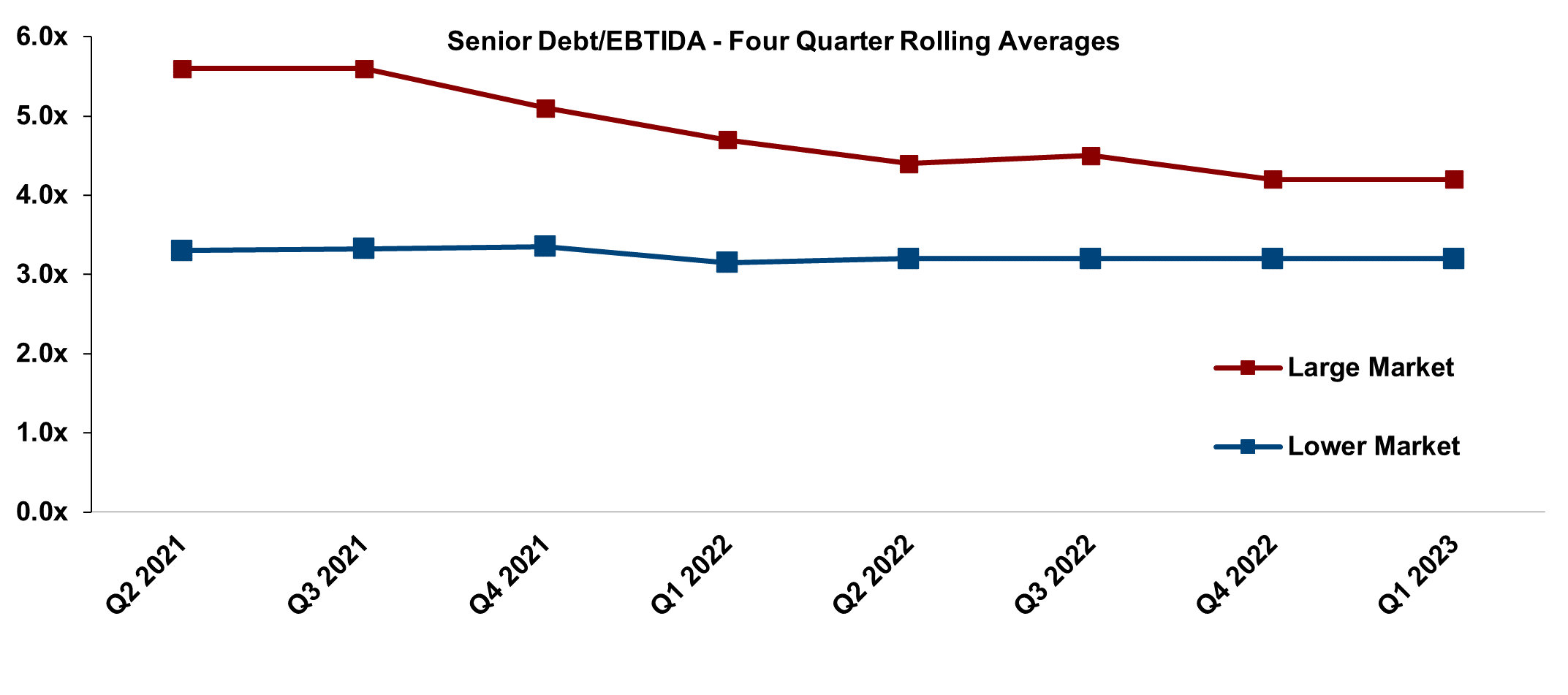

While leverage remains a vital component of M&A, its influence is far from universal. In large deal markets, leverage acts as a double-edged sword, amplifying potential gains and losses alike. The risks and rewards associated with leverage on such a scale demands careful consideration and astute risk management. In periods like today, with higher interest rates and the eminent fear of a recession, the large deal markets have retrenched and lowered transactional leverage rates. This has mollified the volume of M&A activity in the large market.

However, M&A volume, pricing, and activity in the lower market has been less impacted . One of the primary reasons is that leverage has remained stable during the past twelve months. The higher leverage rates and often less accessible non-banks have always been a constraint on market pricing for smaller, privately held companies. However, pricing and deal activity in lower market deals remains robust despite the challenging debt markets.

It is crucial to approach the attention-grabbing headlines in financial publications with a healthy dose of caution. While the large market deals are delayed due to a retrenchment of leverage rates and perceived uncertainties, the lower market deals remain active with modest changes to pricing and leverage rates.

© Copyrighted by Tom Zucker, President of EdgePoint Capital, merger & acquisition advisors. Tom can be reached at 216-342-5858 or on the web at www.edgepoint.com.

Related Insights

-

Selling Without Regret: What Owners Should Know

By John Herubin, Managing Director Most owners spend decades building a company by investing both emotional and financial equity to achieve success. ...

By John Herubin, Managing Director Most owners spend decades building a company by investing both emotional and financial equity to achieve success. ... -

Diversification vs. Specialization: How Buyers Price Machine Shops

By Gary Dagres, Director For owners of precision machining and metal fabrication businesses, one of the biggest questions in a sale process...

By Gary Dagres, Director For owners of precision machining and metal fabrication businesses, one of the biggest questions in a sale process... -

Selling Your Facility Services Company to a Private Equity Platform: What Owners Should Know

By Tom Stafford, Managing Director Across HVACR, Electrical, Plumbing, Roofing, Fire Protection, Landscaping, and other adjacent segments of the Facility Services market,...

By Tom Stafford, Managing Director Across HVACR, Electrical, Plumbing, Roofing, Fire Protection, Landscaping, and other adjacent segments of the Facility Services market,...